The Governmental Accounting Standards Board (GASB) has issued Statement No. 102, Certain Risk Disclosures, to provide users of government financial statements with essential information about risks related to a government’s vulnerabilities due to certain concentrations or constraints. Although this new guidance centers around risk, GASB 102 does not define risk. In fact, the GASB did not spend much time during deliberations discussing what is meant by the term risk, likely because the term risk is already defined in GASB Statement No. 10, Accounting and Financial Reporting for Risk Financing and Related Insurance Issues, which states that risk is “defined variously as uncertainty of loss, chance of loss or the variance of actual from expected results.” Within the context of GASB 102, we can think of risk as the combination of a condition (limited to a concentration or constraint) plus an event, which may result in a substantially negative impact.

Several years ago, the Financial Accounting Standards Board (FASB) issued what is now known as FASB Topic 275, Risks and Uncertainties, which requires certain disclosures about the nature of operations, the use of estimates in the preparation of the financial statements, and significant concentrations. When the GASB deliberated on which FASB guidance to incorporate into GASB literature (GASB 62), it was decided that FASB Topic 275 would not be incorporated until the GASB could assess the requirements considering the government environment. GASB 102 is the result of that assessment or deliberation. It should be noted that most of what is in FASB Topic 275 did not make it into GASB 102. And unlike FASB Topic 275, GASB 102 does not require a disclosure just because a concentration exists.

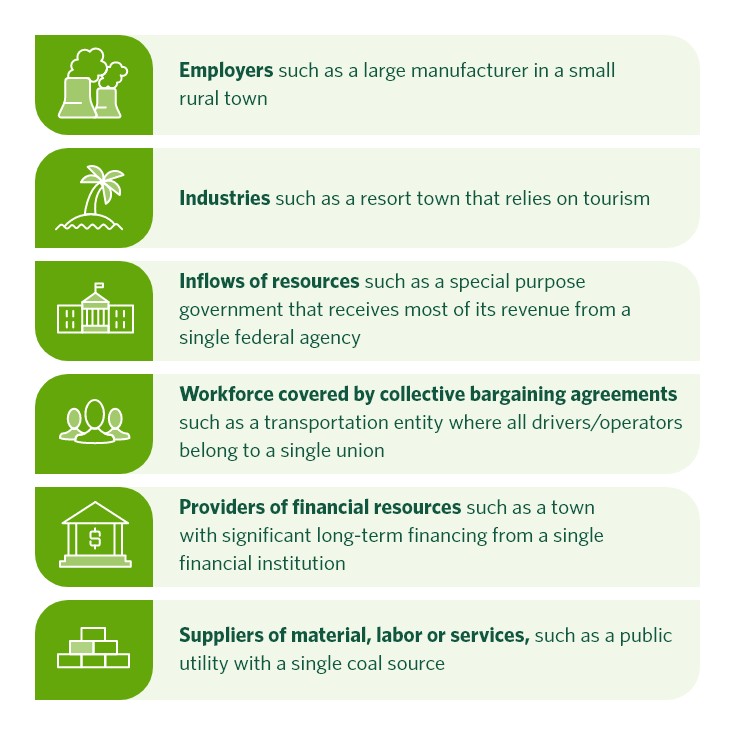

What Is a Concentration and a Constraint, As Defined by GASB 102?

A concentration is a lack of diversity related to an aspect of a significant inflow or outflow of resources. For example, a single employer that employs a majority of the taxpayers in a government’s jurisdiction or a government that relies on one revenue source for most of its funding. Concentrations may include, but are not limited to, the composition of any of the following:

A constraint is a limitation that is imposed by an external party or by formal action of a government’s highest level of decision-making authority. For example, a voter-approved property tax cap or a state-imposed debt limit. Constraints may include, but are not limited to, the following:

When Is GASB 102 Effective?

The requirements of this Statement are effective starting for governments with a fiscal year end of June 30, 2025. Earlier application is encouraged. For most governments, implementation of this guidance will be a non-event, only requiring an internal consideration without an effect on financial reporting. It may be an excellent candidate for early implementation.

What Does GASB 102 Change?

The GASB believes that responsible government officials are already aware of significant concentrations or constraints affecting their jurisdictions. Certainly, GASB 102 is not intended to be the catalyst for bringing such things to their awareness. A government may have a long history of operating with certain concentrations or constraints placed on them. Responsible officials should also already be aware of when an event, or series of events becomes a problem because of the existing concentrations or constraints.

For example, a small town whose primary taxpayer is a large manufacturer will certainly already be invested in keeping said taxpayer within its tax base. News of the manufacturer closing or relocating to a different jurisdiction will be a major concern for the residents of that town. All of this is true without GASB 102. However, what GASB 102 does is require those circumstances to be disclosed in the town’s financial statements. A disclosure is not required when only that concentration exists. A disclosure is required when the event (loss of the taxpayer) is expected to occur in the next year and the effect will be substantial.

Disclosure Criteria

Statement 102 requires governments to disclose a concentration or constraint in the notes to the financial statements if all of the following criteria are met:

- A concentration or constraint is known before the financial statements’ issuance

- The concentration or constraint makes the reporting unit vulnerable to a substantial impact

- An event or events associated with the concentration or constraint that could cause a substantial impact have occurred, have begun to occur, or are more likely than not to begin to occur within 12 months of the date the financial statements are issued

If mitigating actions are taken before the financial statements’ issuance, and they cause any disclosure criteria not to be met, note disclosures are not required.

The application of the disclosure criteria requires the exercise of professional judgement. Nowhere in the GASB literature is the term substantial defined. The GASB believed that prescribing a definition would cause more problems than it would solve. Based on the context of the deliberations, however, substantial can be thought of as more than significant (which is thought to be synonymous with material) but less than severe (possibly catastrophic). Additionally, the likelihood of the impact occurring within the next 12 months also requires professional judgement.

Disclosure in Notes to the Financial Statements

A government should disclose each concentration or constraint that meets the disclosure criteria above in the notes to the financial statements. In its deliberations, the GASB was reluctant to prescribe specific disclosure requirements. The concern with doing so was that governments would limit disclosures to only the minimum requirements and that disclosures would become boilerplate. But the concern with not prescribing disclosure requirements was that governments wouldn’t disclose nearly enough. The spirit of the requirements is that disclosures should provide users with a clear understanding of the nature of the concentration or constraint and its impact. Statement 102 requires the disclosures to describe the following information:

- The concentration or constraint

- Each event associated with the concentration or constraint that could cause a substantial impact if the event had occurred or had begun to occur prior to the issuance of the financial statements

- Actions taken by the government prior to the issuance of the financial statements to mitigate the risk

- Note that future plans would be inappropriate for disclosures and should not be included

Planning for GASB 102 and Beyond

While GASB has identified GASB 102 as a small potential level of effort to implement, having a comprehensive framework to address all upcoming GASB pronouncements is critical for a high-performance state or local government.

Cherry Bekaert has developed a GASB Roadmap checklist that helps track GASB’s assumed level of effort, industry impact, and government available resources to adequately prepare for all upcoming GASB pronouncements and other significant federal and state regulatory issues. For a GASB Roadmap of your own, please reach out to our GASB-as-a-Service professionals.

Related Insights