Introduction

The 2025 PE Pivot From Hesitation to High-stakes Deals

After a shaky start to 2025, U.S. private equity (PE) found its footing. While postelection clarity and pro-business tailwinds promised a rebound, sudden tariff volatility forced a “wait-and-see” pause through the second quarter.

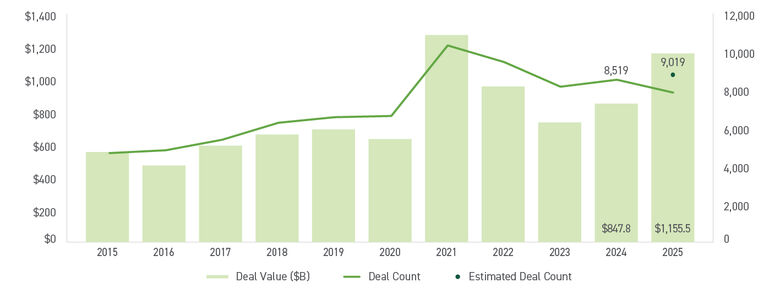

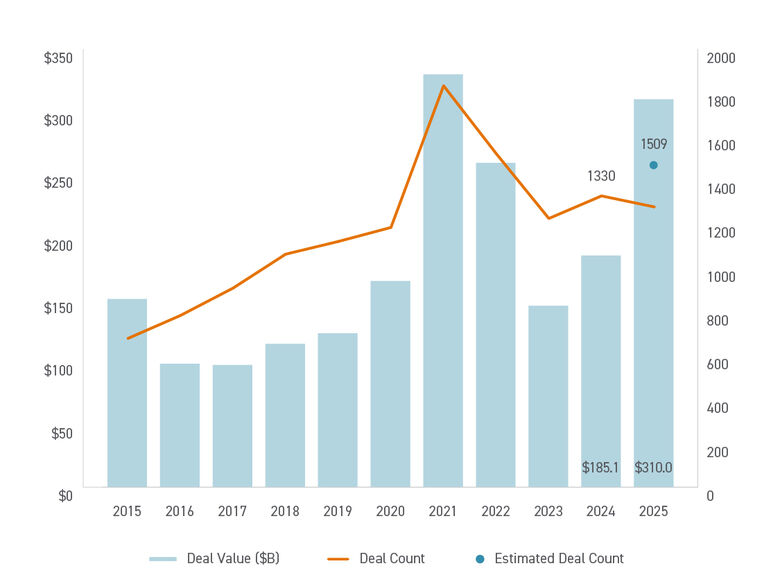

Ultimately, private equity surged to close the year with over 9,000 transactions totaling $1.2 trillion. This marks only the second time in history that annual deal value has crossed the trillion-dollar threshold, rivaling the record-breaking peak of 2021.

Future Outlook: Momentum Meets Opportunity

The stage is set for a strong 2026. With the Federal Reserve’s (Fed) year-end rate cut lowering the cost of capital and dry powder sitting at near records, the momentum from late 2025 is expected to carry forward. Clearer economic skies and more affordable financing mean sponsors are no longer just “window shopping” — they are ready to deploy capital across all sectors. The Fed’s three rate cuts in the back half of 2025 are also likely to support activity into the coming year.

U.S. Private Equity Deal Activity ($B)

Source: PitchBook | Geography: U.S.

As of 12/31/2025

Key Findings

- The Great Rebound: After a tariff-induced Q2 lull, which caused general partners (GPs) to adopt a cautious stance, dealmaking accelerated in H2 as macroeconomic clarity improved and as calculated appetite for risk returned.

- The $1 Trillion Comeback: For only the second time on record, total deal value exceeded $1 trillion with aggregate PE deal value reaching $1.2 trillion across more than 9,000 transactions. This marked a historic milestone previously achieved only during the 2021 peak.

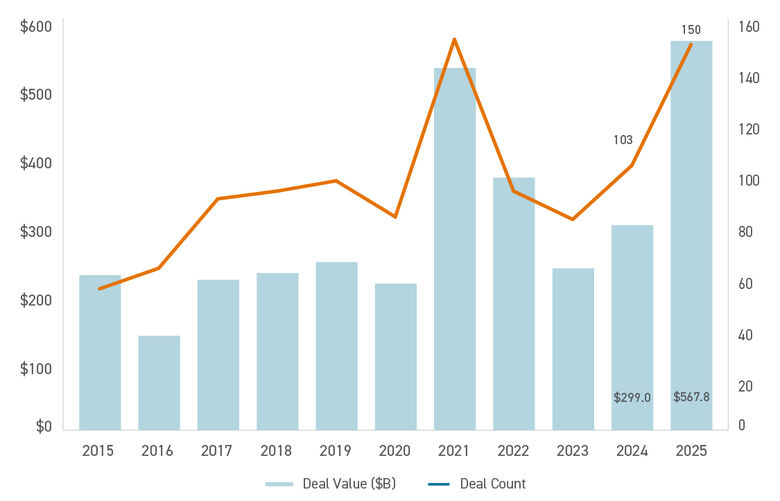

- The “Megadeal” Era: Large-scale transactions ($1B+) reached a record $568 billion in value across 150 deals, signaling massive conviction from sponsors to pursue large, transformative transactions.

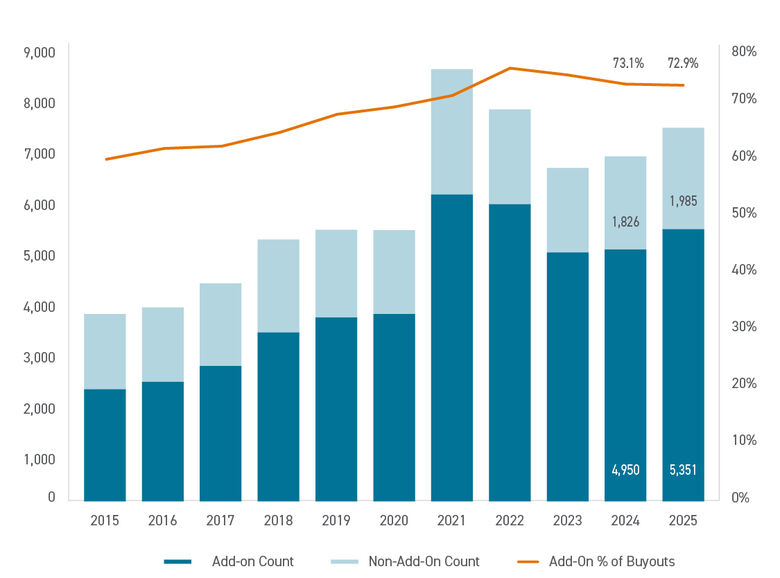

- Add-ons vs. Platforms: At 73% of buyouts, add-ons still dominate the mergers and acquisitions (M&A) market, but easing rates are expected to support greater platform buyout activity and contribute to a modest rebalancing over time.

- Strategic Carve-outs: Corporates are shedding non-core assets, providing fertile ground for PE firms to unlock hidden value from underinvested or noncore corporate assets.

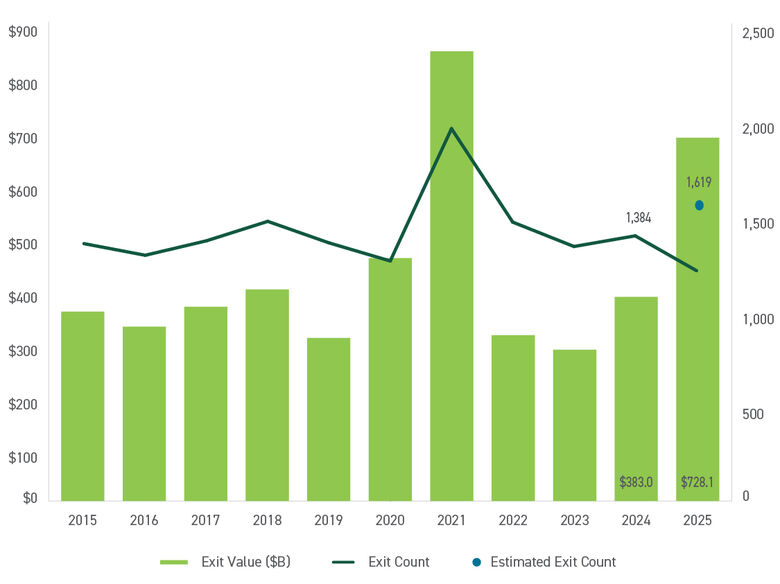

- Exits: After years of stagnation, exit activity surged in 2025. Improved market conditions drove double-digit growth in exit volume, signaling renewed confidence and liquidity.

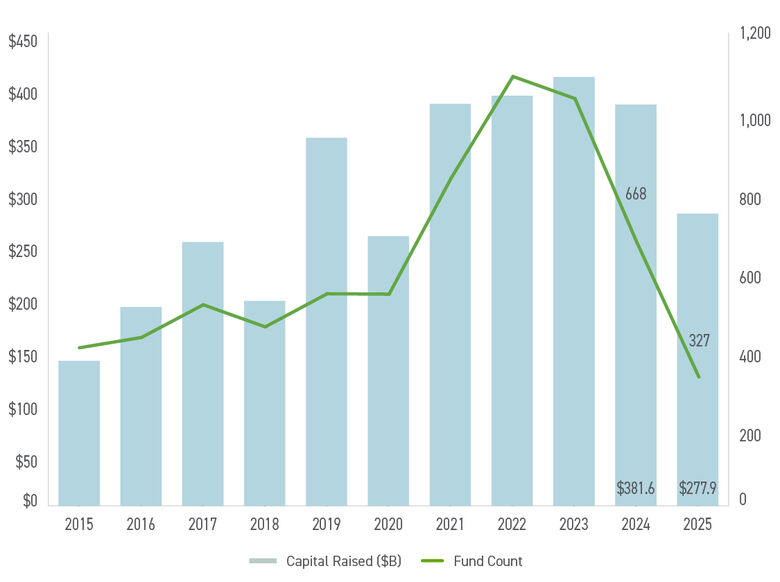

- Fundraising Hits Bottleneck: Capital formation declined year-over-year, making 2025 the weakest year since 2020 — the one dark spot across the PE landscape.

- Dry Powder Maintained Record Levels: Reaching close to $1.1 trillion, current levels of dry powder reflect the imbalance between robust deal activity and subdued fundraising.

- OBBBA Reshapes PE Strategy: Built-in tax incentives favor building and scaling businesses, while reduced limits on interest deductions enhance the effectiveness of highly levered buyouts, pushing firms toward growth-oriented, long-duration investment strategies.

"The surge in PE deal activity in 2025 reset the market, signaling renewed confidence with a growing willingness to transact. Building on 2025's momentum, 2026 will be the year of execution with a focus on accelerating capital deployment, harvesting value through exits and returning capital to LPs."

Trends Across the Private Equity Landscape

Investor Confidence Fuels the High-stakes World of Megadeals

Private equity megadeals, or transactions with enterprise values exceeding $1 billion, played a defining role in shaping market outcomes in 2025. While megadeals turbocharge market totals, they are high-wire acts. Their sheer scale makes them hypersensitive to shifting interest rates and economic tremors, often requiring longer hold periods to prove their worth. To navigate this, sponsors are ditching aggressive debt for conservative leverage, deeper operational playbooks and co-investment structures to spread the risk.

Megadeals emerged as both a catalyst and a consequence of improving macroeconomic conditions, abundant capital availability and evolving sponsor strategies. Their resurgence disproportionately drove aggregate deal value and signaled renewed sponsor confidence.

In 2025, approximately 150 megadeals were completed in the U.S. private equity market, generating total transaction value of roughly $567.8 billion. Although the number of megadeals remained marginally below the record levels observed in 2021, their aggregate value exceeded the 2021 total of $528.2 billion, underscoring the increasing scale and complexity of individual transactions. As a result, megadeals accounted for a substantial share of total PE deal value, elevating overall market volumes to near-record highs.

U.S. Private Equity Deals Over $1B

Source: PitchBook | Geography: U.S.

As of 12/31/2025

The appetite for “big-ticket” deals isn’t going away. With sentiment improving and further Fed rate cuts on the horizon, the environment for massive transactions remains favorable. However, the winners will be those who can maintain valuation discipline and execute complex transformations despite a volatile geopolitical backdrop.

From a market perspective, the dominance of megadeals has contributed to a bifurcation within PE activity. While large sponsors with access to capital and financing benefited disproportionately from favorable conditions, smaller managers faced a more challenging environment marked by limited fundraising success and intensified competition for high-quality, mid-market assets.

Notable Transactions

| Acquirer/ Sponsor(s) |

Target Company | Sector | Deal Value (USD) | Deal Type | Strategic Rationale |

| Thoma Bravo | Boeing’s Digital Aviation Solutions | Aerospace & Defense | $10.5 billion | Corporate Carve-out | Focus on core manufacturing business and improve liquidity. |

| Amber Energy (PE-backed) | Citgo Petroleum (U.S. assets) |

Energy | $7.3 billion | Corporate Carve-out | Acquire scaled refining assets via court-ordered divestiture. |

| Silver Lake-backed Qualtrics (With Co-investors) |

Press Ganey Associates | Healthcare | $6.8 billion | Add-on / Strategic Expansion | Accelerate AI-enabled analytics, expand healthcare and enterprise insight capabilities. |

| Clearlake Capital | ModMed | Healthcare Technology | $5.3 billion | Buyout | Growth acceleration of AI-enabled software solutions. |

| RedBird Capital Partners & Mubadala Investment Company-backed Aquarian |

Brighthouse Financial | Financial Services | $4.1 billion | Platform Acquisition | Strengthen exposure to U.S. retirement and annuities market. |

| Warburg Pincus and Berkshire Partners | Triumph Group, Inc. | Industrial | $3.0 billion | Take Private | Capitalize on Triumph’s portfolio optimization as a premier aerospace components provider. |

| Tinicum & Blackstone | TriMas Aerospace | Aerospace & Defense | $1.45 billion | Corporate Carve-out | Portfolio optimization for seller; platform growth opportunity for sponsors. |

Source: PitchBook | Geography: U.S.

As of 12/31/2025

Exit Activity Surges Amid Improving Market Conditions

After years of “wait-and-see,” the exit market finally roared back to life in 2025. Following an era of extended hold periods and valuation stalemates, the industry achieved double-digit year-over-year growth in exit volume for the first time in four years. Until recently, exit volumes remained subdued as valuation uncertainty led PE firms to extend hold periods, with relatively few assets achieving exits at attractive pricing.

The growth in exit counts signals improved liquidity and greater asset turnover. While the high end of the market is moving fast, the focus now shifts to the broader inventory of PE-backed assets. The “logjam” is breaking, but the pace of the total recovery will depend on whether this newfound exit flow holds steady through the coming months.

U.S. Private Equity Exit Activity ($B)

Source: PitchBook | Geography: U.S.

As of 12/31/2025

Fundraising Friction: Capital Remains the Final Frontier

In a year of record dealmaking, fundraising was the glaring outlier. While deal and exit volumes soared in late 2025, capital formation hit a wall, making it the weakest fundraising year since 2020. We are currently witnessing a historic “structural disconnect” between the abundance of investment opportunities and the scarcity of new commitments.

The fundraising slowdown was evident in both the number of funds closed and the total amount of capital raised. Year-over-year declines in fund count reflected limited partner (LP) caution as well as strategic decisions by GPs to delay or postpone fundraising efforts in anticipation of more favorable conditions. Some managers opted to extend existing funds or rely on continuation vehicles and co-investments rather than launch new flagship vehicles into a challenging fundraising environment.

U.S. Private Equity Fundraising Activity ($B)

Source: PitchBook | Geography: U.S.

As of 12/31/2025

Despite a public market recovery, many LPs (pensions, endowments and insurers) remain overallocated to private equity, leaving little room for new commitments. Constrained capital availability has led LPs to play it safe by concentrating commitments among established GPs and larger, multi-strategy platforms with proven track records, often at the expense of smaller or emerging managers.

Importantly, managers that successfully raised capital generally did so within historical fundraising timelines, suggesting that the primary constraint was access to capital rather than prolonged fundraising processes. This trend has contributed to the continued accumulation of dry powder which reached a record high of $1.1 trillion, although this balance is expected to decline as deal activity continues to outpace new capital formation.

In addition, slower-than-expected distributions from private equity funds further constrained LP liquidity. While exit activity increased year-over-year, it had not yet reached a scale sufficient to materially improve the recycling of capital back to investors.

The Strategy Playbook: Add-ons and Carve-outs

While megadeals grab the headlines, the “engine room” of 2025 was defined by two proven strategies: the relentless scaling of existing platforms via add-on deals and the surgical extraction of corporate gems.

Add-ons: The Dominant (But Shifting) Force

Add-on acquisitions accounted for 72.9% of all buyouts in 2025, holding steady with the five-year average. By bolting smaller companies onto existing platforms, GPs continue to grow and build resilience.

While add-ons continue to represent a dominant share of buyout activity, this elevated level is expected to moderate gradually as financial conditions become more accommodative. In particular, a sustained decline in interest rates is likely to stimulate broader deal activity — especially leveraged platform buyouts — which may produce a modest crowding-out effect and result in a slight reversion of add-ons toward historical norms.

The persistence of above-trend add-on activity reflects clear strategic and economic rationales. Larger, integrated platforms created through add-on acquisitions benefit from enhanced purchasing power, enabling more efficient resolution of supply chain challenges and the ability to spread cost efficiencies across a wider revenue base. Increased scale also provides greater financial resilience during economic downturns and, in less competitive market environments, affords firms enhanced pricing power to support margin stability.

Several notable transactions illustrate these dynamics. Among the largest add-on deals of the year was Qualtrics’ $6.8 billion acquisition of Press Ganey Associates, a provider of strategic advisory services focused on patient safety and care quality. Backed by Silver Lake and other sponsors, Qualtrics expects the transaction to accelerate the deployment of artificial intelligence (AI) capabilities and strengthen its ability to deliver value across a broad range of industries.

In the financial services sector, Aquarian, supported by RedBird Capital Partners and Mubadala Investment Company, agreed to acquire Brighthouse Financial for $4.1 billion. This acquisition aligns with Aquarian’s strategic emphasis on the U.S. retirement market, which represents a significant long-term growth opportunity for the platform.

Add-ons as a Share of All U.S. Private Equity Buyouts

Source: PitchBook | Geography: U.S.

As of 12/31/2025

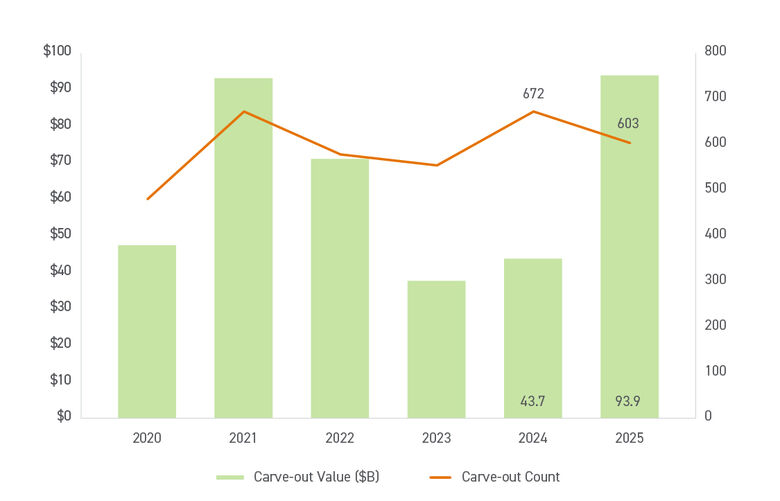

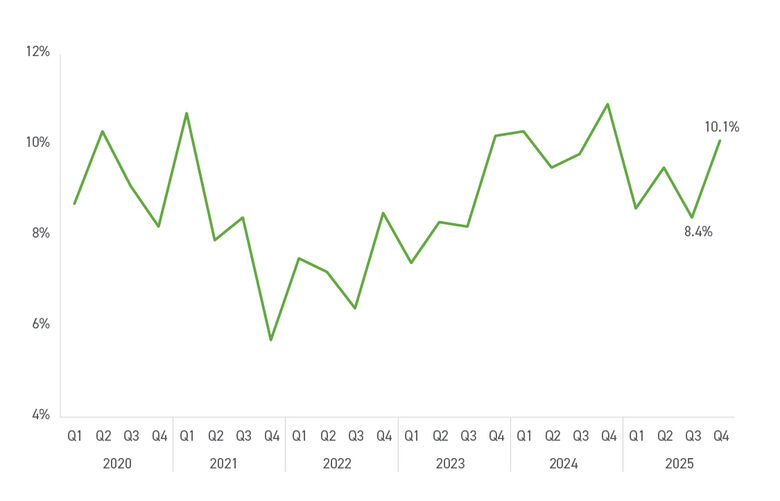

Carve-outs: Unlocking Hidden Gems

Corporate carve-outs — buying a “piece” of a larger company — remained a favorite for both sponsors and sellers. In a stabilized rate environment, this became a win-win strategy. For corporate sellers, a carve-out can present a portfolio detox through divesting non-core or underperforming business units, which allows corporations to sharpen their strategic focus, improve capital efficiency and present a more compelling investment narrative to shareholders.

"Corporate sellers continue shedding non-core segments to improve balance sheet measures and enhance focus on core business activities. No longer just a tactical exit, carve-outs provide sponsors strategic transformation opportunities. Top-tier operators win by mastering the ability to decouple a business from its parent without losing operational momentum or talent.”

U.S. Private Equity Carve-out Activity ($B)

Source: PitchBook | Geography: U.S.

As of 12/31/2025

For sponsors, this strategy is often seen as a de-risked opportunity. Absent the entanglement challenges from the parent company, carve-outs generally come with well-established operating histories, which allow for greater visibility into opportunities to improve future profitability trends leading to more confident underwriting of valuations.

Carve-outs/Divestitures as a Shared of All U.S. Private Equity Buyouts

Source: PitchBook | Geography: U.S.

As of 12/31/2025

In many cases, divested assets exhibit underperformance not due to fundamental weaknesses, but rather because of limited managerial attention or capital investment under prior corporate ownership. Similar to founder-owned enterprises, such assets often present multiple value-creation levers for sponsors, including operational optimization, strategic repositioning and accelerated growth initiatives following separation.

Although carve-outs did not match the historically high share of buyout activity recorded in 2024, their proportion declined to 8.5% in the first quarter of 2025 before recovering to slightly above 10% by the end of the fourth quarter. This rebound places carve-out activity above both the five-year quarterly average of 8.6% and the level observed in the third quarter, underscoring their sustained relevance within private equity dealmaking strategies.

Notable transactions in the fourth quarter illustrate this continued momentum. Citgo agreed to sell its petroleum business to PE-backed Amber Energy for $7.3 billion following a court-ordered auction approved by a U.S. federal judge, arising from outstanding debt obligations owed by Venezuela, Citgo’s ultimate owner. In addition, TriMas announced the sale of its TriMas Aerospace division to Tinicum and Blackstone for $1.45 billion after a strategic review by its board to optimize portfolio composition and unlock shareholder value.

Technology Sector

Selective Scale-up of Cash-generative Platforms Drives Growth

Technology continued to be one of the most active sectors for private equity in 2025, accounting for the largest share of PE deal activity by value, with approximately 25% of all private equity-backed transactions attributed to this sector by late 2025. This emphasized sponsors’ sustained interest in high-growth and scalable technology businesses, even amid broader market headwinds.

PE deal activity in technology exhibited strong value dynamics. According to broader PE metrics, U.S. deal value climbed substantially in 2025, with tech integral to that trend. Technology’s relative resilience was reflected in heightened transaction values even as overall deal volume softened in some parts of the market.

U.S. Technology Private Equity Deal Activity ($B)

Source: PitchBook | Geography: U.S.

As of 12/31/2025

Several headline transactions highlighted the strategic gravitation toward technology and adjacent tech-enabled sectors. Notably, software and analytics firms with strong recurring revenue, particularly those leveraging AI, attracted significant sponsor capital. For example, Thoma Bravo, a major software investment firm, acquired Verint Systems for $2 billion in late 2025 and immediately merged it with its portfolio company, Calabrio, to create a leading, combined force in AI-powered customer experience (CX) automation, aiming to offer a comprehensive, end-to-end platform for enterprises.

This deal, emblematic of larger technology buyouts in 2025, underscored private equity’s emphasis on platform expansion, integration of artificial intelligence capabilities, and value creation through cross-sector strategic positioning.

Within technology, subsectors such as cybersecurity, healthcare technology (healthtech), and enterprise software saw meaningful PE deal flow. In the cyber space, there was a strong wave of smaller, targeted acquisitions in identity, authentication and governance platforms, with dozens of transactions clustered in late 2025, reflecting sponsors’ priorities on mission-critical digital security capabilities.

Consolidation in healthtech also surged as PE firms pursued scalable technology solutions for telehealth, data analytics and digital patient care platforms. This activity was driven both by strategic synergies and by maturation among venture capital (VC)-backed technology assets entering the buyout consideration set.

U.S. Cybersecurity Private Equity Deal Activity

Source: PitchBook | Geography: U.S.

As of 12/31/2025

These consolidation waves were characterized not only by scale, but by strategic integration aimed at building broader platforms with compelling growth trajectories and resilient recurring revenues.

While other sectors faced an exit bottleneck, technology assets found their way to the finish line. High interest from both strategic corporate buyers and fellow sponsors (sponsor-to-sponsor) kept liquidity flowing. In fact, mid-summer tech exits contributed a disproportionate share of the year’s total exit value, proving that high-quality tech remains the market’s most liquid currency.

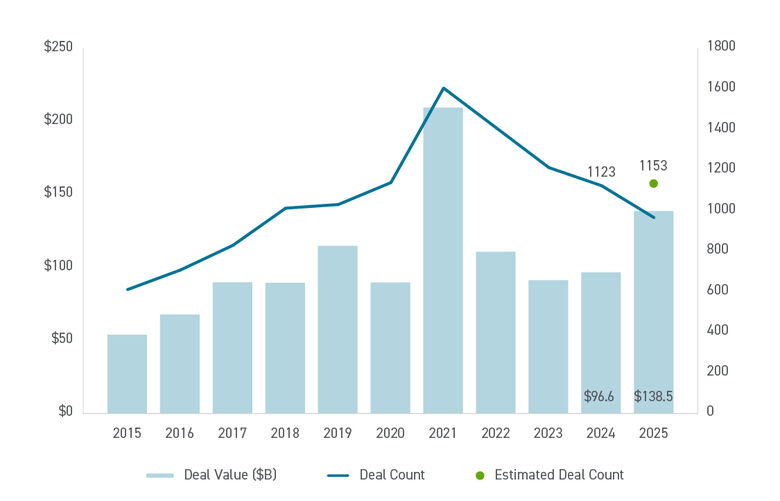

Healthcare Sector

Near Record-breaking $140 Billion Pulse

Healthcare private equity went beyond simply recovering in 2025; it hit a new gear. With a staggering 45% increase in deal value over the previous year, the sector proved that demographic tailwinds and digital transformation are a potent mix for investors.

U.S. Healthcare Private Equity Deal Activity ($B)

The sector experienced a record surge in deal value, with transactions totaling an estimated $140 billion on 1,153 total transactions. This performance was bolstered by a meaningful rebound in large transactions, including a substantial increase in deals with enterprise values exceeding $1 billion. Within that total, PE sponsors announced approximately 33 buyouts — the second-highest yearly count on record — to reflect strengthened sponsor confidence and renewed deal pipelines that had been postponed in prior years.

Private Equity’s Key Strategic Orientation in Healthcare

- Healthcare IT and Digital Platforms: Sponsors placed increased emphasis on technology-enabled solutions, such as electronic health record interfaces, revenue cycle management systems, AI-driven care delivery platforms and workforce optimization technologies. These areas were seen as drivers of downstream operational efficiencies and cost resilience.

- Provider Services Consolidation: Physician practices, outpatient care networks and specialty care groups remained attractive targets due to their recurring revenue profiles and consolidation potential. Roll-up strategies continued to be a key playbook for expanding scale and geographic reach.

- Non-core Carve-outs and Divestitures: Health systems and healthcare conglomerates increasingly pursued divestitures of non-core units, such as lab services or administrative support functions, creating acquisition opportunities for private equity sponsors.

Exit activity in the healthcare sector in 2025 also rebounded significantly from prior years, signaling improved liquidity and confidence in monetizing mature assets. Healthcare exit value was estimated at roughly $156 billion, well above the $54 billion seen in 2024.

The resurgence of sponsor-to-sponsor exits and broader exit pathways, such as secondary sales and strategic acquisitions, helped sponsors recycle capital and support ongoing deal activity. This exit rebound was instrumental in offsetting earlier exit delays and improving the overall return profile for LPs.

Collectively, the performance of healthcare PE in 2025 positions the sector well for continued momentum in 2026. High levels of dry powder, improving exit pathways and a maturing pipeline of sponsor-owned assets nearing optimal harvest points are expected to sustain transaction activity. Moreover, ongoing secular trends in aging demographics, digital transformation and therapeutic innovation are likely to bolster long-term sponsor interest across subsegments of healthcare.

"Healthcare PE activity is rebounding with a “flight to quality,” as investors deploy record levels of capital into scalable niches like behavioral health, value-based care and AI-enabled pharma services. This momentum stems from consolidating fragmented physician groups into efficient outpatient models using digital tools to drive margin expansion. However, growth is tempered by tightening regulatory scrutiny, labor inflation and the rising cost of clinical cybersecurity.”

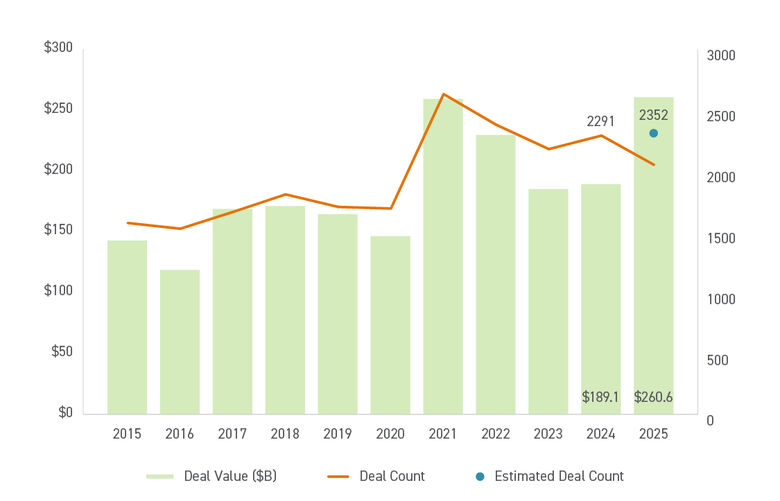

Industrial Sector

Scale, Automation and Supply-chain Resilience Highlights Performance

The industrials sector saw valuations rising in 2025, as PE deal value rose 37.8% year-over-year, reaching $260.6 billion and up from $189.1 billion in 2024. Deal count also rose, but much more moderately, with a 2.7% increase to 2,352 deals in 2025, versus 2,291 in 2024. This elevated level of investment reflects ongoing interest from sponsors in assets tied to infrastructure, capital equipment, supply chains and advanced production capabilities.

Despite a turbulent year with ups and downs related to tariffs, inflation and interest rate uncertainties, dealmaking in the industrials sector remained resilient. In fact, it appears to have benefited from the slow downward progression of interest rates, even if they did not fall as fast as predicted toward the end of 2024.

In addition, dealmaking picked up after tariff uncertainty eased, as industrial PE investors became less uncertain about the direction of the economy and the impact of these levies. The surge in private credit kept markets liquid and fueled many deals that might not have been financed otherwise.

U.S. Industrials Private Equity Deal Activity ($B)

Source: PitchBook | Geography: U.S.

As of 12/31/2025

A number of notable industrial transactions in 2025 demonstrate how private equity engaged with strategic assets, including industrial-equipment maker SPX Flow’s, owned by Lone Star Funds, agreement to be acquired by ITT for nearly $4.8 billion. Although this was a sale to a strategic buyer, it highlights the scale of industrial platforms that private equity has previously built and positioned for monetization.

Private equity activity also included sponsor-to-sponsor exits in industrial subsegments, exemplified by KKR’s sale of aerospace parts supplier Novaria Group to Arcline Investment Management for about $2.2 billion, which reflects continued secondary transactions in industrial components and defense-linked manufacturing.

These deals underscore the scale and strategic positioning that PE can bring to industrial assets, often enhancing operational capabilities and pursuing growth before exiting into strategic acquirers or other financial sponsors.

Strategic Themes Driving PE Interest in Industrials

Private equity investors in the industrials sector were intrigued by mega themes that made the space more attractive, including:

- Reshoring and Supply-chain Resilience: Sponsors increasingly targeted businesses positioned to benefit from reshoring trends and supply chain localization. This included manufacturers and component producers serving domestic markets, as companies across sectors sought to reduce dependency on overseas supply chains, a trend supported by larger policy and capital expenditure initiatives.

- Technology Modernization and Automation: Industrial companies that integrated automation, digital manufacturing technologies, AI, robotics or operational analytics were especially attractive. Priorities for investors also include data centers fueling infrastructure and construction activity, as well as aerospace and defense sector projects that benefit from strong funding and demand. Enhancing productivity and cost efficiency through modern equipment and predictive systems appealed to sponsors as a value creation lever.

- Operational Resilience Amid Volatility: Given macroeconomic uncertainties, targets with stable cash flows, diversified customer bases and strong defensive characteristics remained priorities. Sponsors showed a willingness to structure deals that reflect both growth potential and resilience to cyclical downturns.

Looking ahead, despite ongoing economic and policy uncertainty, the fundamentals supporting private equity interest in industrial and manufacturing assets — including fragmentation, operational transformation potential and long-term domestic investment — remain compelling. Reasonable valuations, availability of dry powder and a more favorable interest rate environment should fuel another strong year in industrials dealmaking.

"Fueled by the surge in AI/data centers, tax reform and the reshoring renaissance, the next era of energy and industrial M&A belongs to architects of transformation. Success no longer hinges on the entry price, but the investor’s ability to forge scalable powerhouses with bulletproof cash flows that can weather any macroeconomic volatility.”

Professional Services Sector

Boring Becomes Beautiful

Professional services sector M&A — encompassing accounting and CPA firms, wealth and asset management, financial advisory platforms, and consulting businesses — thrived from investors’ focus on essential, recurring cash flows, significant consolidation opportunities in fragmented sectors, and technology advancement implementations in historically slow-to-change businesses. Even as overall deal volume across the broader PE market showed selectivity and concentration in larger transactions, activity in the professional services sector continued to be a bright spot in 2025.

CPA Firms: The PE Transformation of Accounting

One of the most active areas within professional services was the accounting and CPA segment. Private equity investment accelerated in 2025 as sponsors doubled down on consolidation of a highly fragmented industry with predictable demand and strong recurring revenues. By many industry trackers’ estimates, more than 50 PE-related transactions occurred in the CPA and accounting sector through 2025, significantly outpacing prior years and reflecting an accelerating PE footprint in the profession. As of early 2026, almost half of the top 30 CPA firms in the U.S. have some form of PE investment or alternative practice structure (APS). The pace in the sector is only expected to continue.

This represents a massive shift in the industry; just five years ago, PE investment in the sector was almost nonexistent. The trend is largely driven by the opportunity for massive capital to invest in technology infrastructure and support growth through acquisitions of smaller firms.

Notably, in early 2025, New Mountain Capital sold Citrin Cooperman to Blackstone, representing the first top 30 CPA firm in the country to successfully transfer private equity ownership in a sponsor-to-sponsor transaction. Reportedly at roughly a $2 billion valuation, the deal demonstrated a viable exit path for a scaled PE-backed platform, as well as continued interest and opportunity in the market at scale.

Selected Recapitalization Transactions Across Top 30 CPA Firms1

| Rank2 | Firm Name | PE Investor(s) | Year Initial Deal Announced |

| #6 | Baker Tilly | Hellman & Friedman / Valeas Partners | 2024 |

| #7 | CBIZ | N/A (public listing) | 1996 |

| #8 | BDO USA | Apollo (alternative financing via ESOP) | 2023 |

| #9 | Grant Thornton | New Mountain Capital | 2024 |

| #14 | CohnReznick | Apax Partners | 2025 |

| #15 | EisnerAmper | TowerBrook Capital Partners | 2021 |

| #16 | Citrin Cooperman | Blackstone (formerly backed by New Mountain Capital) | 2022/2025 |

| #18 | Andersen | N/A (public listing) | 2025 |

| #17 | Eide Bailly | Sequoia Financial (strategic investment) | 2024 |

| #19 | Armanino | Further Global Capital | 2024 |

| #20 | Cherry Bekaert | Parthenon Capital | 2022 |

| #23 | Carr, Riggs & Ingram | Centerbridge Partners / Bessemer | 2024 |

| #24 | Aprio | Charlesbank Capital Partners | 2024 |

| #25 | Sikich | Bain Capital (minority investment) | 2024 |

| #26 | PKF O’Connor Davies | Investcorp / PSP Investments | 2024 |

Source: 1CPA Trendlines, As of 1/31/2026

2INSIDE Public Accounting, As of 10/31/2025

"Professional Services is PE’s new frontier for scale. Sponsors are aggressively consolidating fragmented sectors — leveraging AI and bolt-on acquisitions to turn predictable cash flows into tech-enabled powerhouses.”

Wealth Management: RIA Roll-up Gold Rush

Private equity interest in wealth and financial advisory businesses also remained strong in 2025, driven by the sector’s fragmented structure, growth in assets under management (AUM) and recurring fee models. Sponsors continued to pursue transactions across wealth management, financial planning and financial technology platforms that support advisors and institutions.

Examples include GTCR’s acquisition of FMG Suite, a marketing and software platform for financial advisors, which highlights PE’s strategic interest in tools that enhance client engagement and operational efficiency for advisors. Separately, the sale of Aon’s wealth unit back to Madison Dearborn Partners for $2.7 billion showed private capital’s willingness to invest in established advisory businesses and reposition them for scale, even in a complex transaction environment.

Across the broader asset management value chain, PE deals in wealth and asset management continued to benefit from sponsors targeting mid-market firms with strong client retention, recurring revenues and potential for digital enablement. Although the data for 2025 is still emerging, the trend suggests sustained PE participation in asset management segments as firms seek consolidation and platform expansion opportunities.

Consulting and Advisory: People-powered Platform Investing

The consulting subsector — including management consulting, risk advisory and specialty business services — also remained an area of private equity activity in 2025, although deal volumes and sizes varied more than in accounting and wealth segments.

Private equity was active in advisory businesses with technology-enabled service offerings, niche specializations or consultancy practices aligned with growth sectors (e.g., digital transformation, compliance and risk). Broader transaction data for business and professional services show that this sector accounted for a meaningful share of PE deals, capturing nearly 19% of private equity transactions in the third quarter of 2025 across all industries.

Going into 2026, private equity activity in professional services is expected to remain dynamic, though sponsors will likely remain selective amid broader fundraising challenges and competitive pressure for high-quality assets. Key expectations include:

- Continued investments in accounting and CPA firms, with further platform consolidations, bolt-on acquisitions and minority stake transactions.

- Private equity may begin exiting many of its earliest professional services platforms, given the number of platform deals over the past four years and the success these investments have had in generating scale while improving profitability.

- Growth in wealth and advisory platforms, particularly where technology integration can enhance client acquisition and retention.

- Strategic consulting investments where firms offer differentiated, high-value advisory services or tech-enabled solutions.

Overall, professional services remained an important and resilient segment of private equity investment activity in 2025, driven by structural trends, stable demand, and the ability to build larger, integrated service platforms through capital and operational expertise.

Other Sectors To Watch

Consumer and Residential Services: Poised for Transformation Beyond Consolidation

The consumer and residential services sector, often referred to as field services, continued to attract significant private equity interest in 2025, driven by secular demand resilience, fragmentation, recurring revenue potential, and value creation opportunities through platform roll-ups and operational transformation.

These services are underpinned by stable demand, as homeowners and commercial property owners alike continue to require maintenance and repair regardless of broader economic conditions. According to industry analysis, this category represents a hundred billion dollar market with double-digit growth rates, underlining its appeal to capital providers seeking recession-resilient investment opportunities.

The fragmented nature of the market, with tens of thousands of mostly small, founder-led operators, creates natural opportunities for consolidation through PE-led platform strategies. A high proportion of operators remain independent, making them attractive targets for add-on acquisitions and regional scaling.

"Private equity remains aggressive in consumer and residential services, where essential, needs-based demand acts as a natural hedge against volatility. By applying a proven operational playbook — focused on transformation and platform scaling — sponsors are rapidly modernizing their consumer and residential services platforms.”

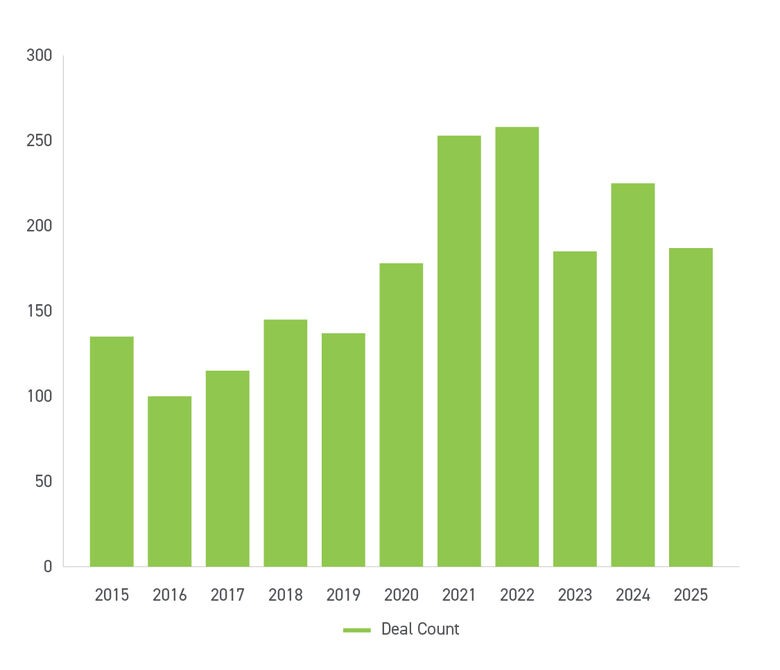

U.S. Consumer and Residential Services Private Equity Deals Since 2024

Source: PitchBook | Geography: U.S.

As of 1/30/2026

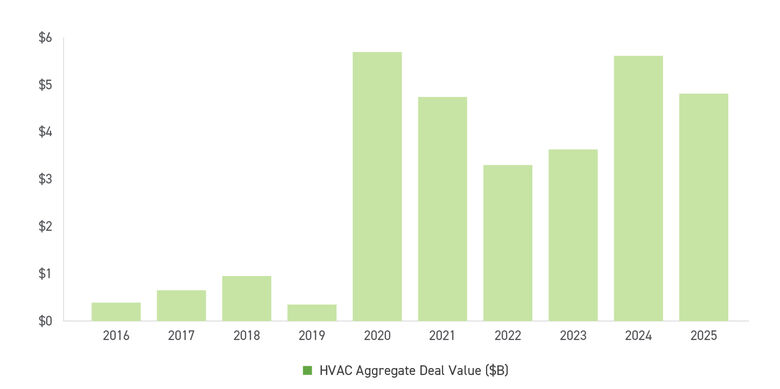

HVAC services continued to be a major focus of PE investment in 2025, despite a small dip in aggregate investment capital. PE firms and their portfolio companies accounted for a majority of transactional activity in HVAC M&A, which demonstrates the continued appetite for roll-ups and platform expansion in this subsector.

HVAC Private Equity Aggregate Deal Value ($B)

Source: PitchBook | Geography: U.S.

As of 1/30/2026

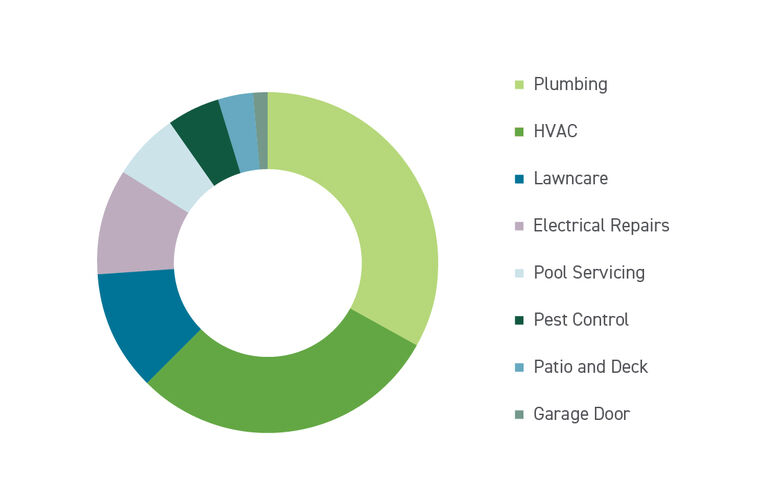

Mid-market providers, especially those with recurring maintenance revenue and broad service footprints, attracted greater attention from financial sponsors as potential platforms for scale.

Beyond HVAC, transaction activity also extended into other home services segments such as plumbing, pest control and landscaping, though deal volumes in those subsectors varied more by region and sponsor strategy.

Several large and strategically significant transactions signal PE’s continuing engagement in field services in 2025:

- Blackstone’s acquisition of Shermco, a provider of electrical testing and maintenance services, from Gryphon Investors for approximately $1.6 billion. Although focused on electrical systems services broadly, this deal highlights investor interest in service-oriented maintenance and engineering platforms that serve both residential and commercial markets.

- CenterOak Partners’ sale of Turf Masters Brands, Inc., a leading provider of residential recurring lawn, tree and shrub care services, to ExperiGreen Lawn Care.

- CCMP Growth Advisors’ acquisition of Airo Mechanical, a prominent provider of HVAC and plumbing services, further illustrates active mid-market activity and strategic consolidation in essential service specialties.

- Sentinel Capital Partners’ sale of an HVAC division of NSI Industries to Lennox International for $550 million reflects continued sector consolidation and sponsor realization of value.

Beyond individual deals, new funds focused on industrial and services assets, such as the $400 million debut fund raised by Point 41 Capital Partners targeting lower mid-market industrial and services deals, signal sustained investor confidence in field services as a durable opportunity set.

The trends that shaped 2025 PE activity in field services suggest continued strategic expansion and consolidation. Overall, PE deal activity in the consumer and residential services sector has demonstrated durable momentum and strategic refinement, as sponsors continue to deepen investments in field services platforms and deploy sophisticated value creation playbooks to build scale and competitiveness in core service categories.

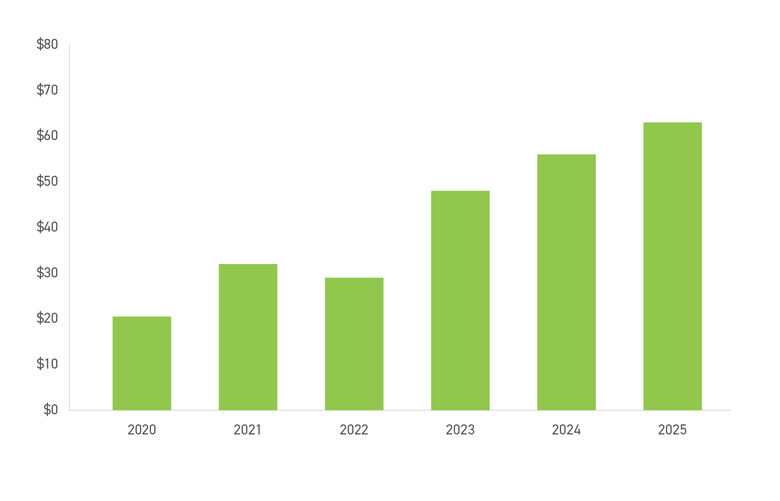

Financial Services: A Safe Haven With Steady Yields

PE activity in the U.S. financial services sector remained active and strategically significant, even as overall deal volume faced headwinds tied to macroeconomic uncertainties and a broader slowdown in fundraising. Financial services — including insurance, banking, asset management, private credit and other specialized finance platforms — continued to attract substantial sponsor attention, driven by stable fee-based revenues, fragmentation, regulatory evolution and opportunities for consolidation.

Even amid a generally softer overall PE market in the first half of the year, financial services maintained a prominent role in transaction activity. Sector deals were diverse in structure, ranging from buyouts and growth capital to strategic acquisitions and carve-outs, and reflective of the broad set of subsegments within financial services that are attractive to sponsors. This trend was consistent with broader M&A data showing strong financial services dealmaking overall in 2025 across all buyers, including corporations and financial sponsors.

Private Equity Investments in Finance Services ($B)

Source: PitchBook | Geography: U.S.

As of 1/30/2026

The insurance and retirement services subsector demonstrated significant activity. One of the most notable PE-influenced transactions in 2025 involved the acquisition of Brighthouse Financial, a major U.S. life insurer and annuity provider, by Aquarian Capital and its sponsors for approximately US $4.1 billion. This transaction underscores sponsors’ appetite for stable, capital-light insurance platforms with attractive cash flows and exposure to retirement and annuity markets, two segments expected to benefit from demographic tailwinds and predictable revenue streams.

Historically, insurance and retirement services assets have been attractive to private capital due to their long-duration liabilities, recurring premium or fee income, and potential for operational improvement through product rationalization, pricing refinement and balance sheet optimization.

While not always classified strictly within traditional financial services, private credit, fund administration and related services also saw notable sponsor activity. Financial sponsors continued to support private credit growth, often as part of portfolio diversification and to capture direct lending opportunities as traditional banks retrenched from certain lending segments. This shift reflects broader marketize reliance on private credit for leveraged financing and specialty financing solutions.

Historical activity in fund services businesses, such as GTCR’s prior transaction involving fund administration platforms, demonstrates how sponsors view financial infrastructure businesses as attractive, recurring revenue generating assets.

Looking forward, private equity activity in the financial services sector is expected to remain resilient but selective. Growth in wealth and asset management platforms is likely to continue as aging demographics, and demand for personalized advice, expand AUM bases. Insurance assets, especially specialty lines and annuity providers, will remain attractive, particularly for sponsors willing to navigate actuarial, regulatory and capital optimization complexities. Financial infrastructure and private credit segments may benefit from ongoing bank retrenchment and increasing use of alternative financing by mid-market firms.

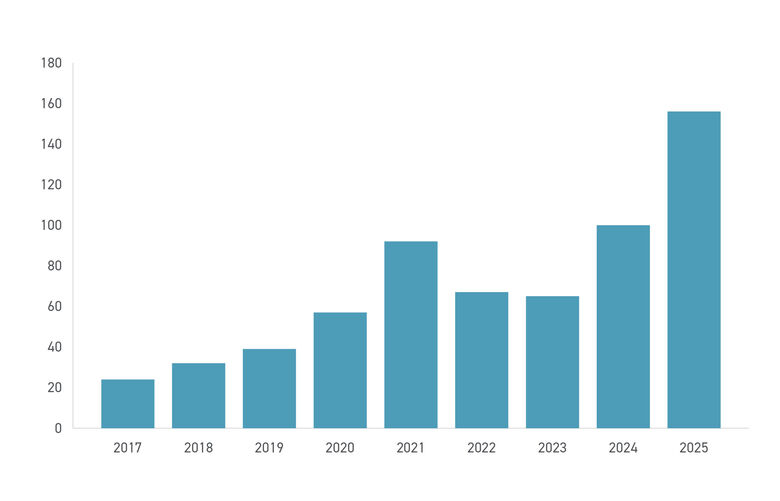

AI and Machine Learning: Cutting-edge Tech and Infrastructure Signal Opportunity

In 2025, AI continued to dominate the investment landscape, with the U.S. at the forefront of global activity. PE participation in AI increased sharply as firms deployed capital into infrastructure, AI-enabled platforms and machine learning businesses with strong growth potential. According to PitchBook data, the U.S. captured a significant share of global AI deal value, with about 79% of AI funding going to U.S.-based companies in 2025, cementing the country’s leadership in this technology domain.

Although comprehensive PE-specific tallies are less centralized than VC data, broader analysis suggests that private equity firms drove a substantial portion of large later-stage and infrastructure deals, which aggregated billions of dollars in deployments across AI infrastructure, applied AI platforms and strategic acquisitions.

Private Equity Investments in AI (#)

Source: PitchBook | Geography: U.S.

As of 12/31/2025

PE involvement in AI in 2025 was marked by a shift to larger deals and infrastructure-focused investments. Large institutional investors and PE sponsors participated in multibillion-dollar infrastructure acquisitions that are foundational to AI development. For example, a consortium including BlackRock, Microsoft and Nvidia agreed to buy Aligned Data Centers for $40 billion, a deal that extended beyond traditional PE (involving strategic partners) and highlighted the scale of investor commitment to AI computing infrastructure.

Firms with a strong balance sheet and dedicated AI or technology funds, including emerging specialty players backed by institutional capital, planned or executed significant investments. This signaled that AI had evolved from an early-stage, venture-dominated theme to a core strategic axis for mid- and later-stage private equity deployment. These infrastructure investments illustrate that PE’s approach to AI in 2025 increasingly encompassed software and algorithms in addition to the essential compute and data backbone required for large-scale AI models and services.

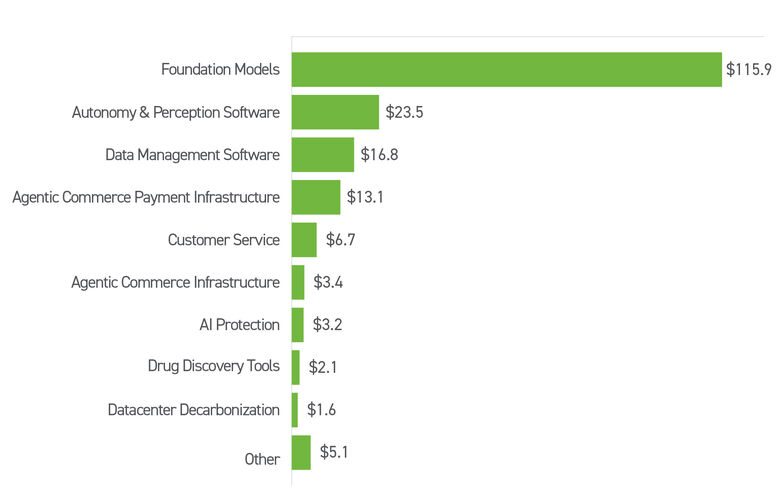

Top AI Subsectors by Capital Invested ($B) From 2022 to 2025

Source: PitchBook | Geography: U.S.

As of 10/31/2025

Legislative Update

OBBBA Tax Incentives Reshape Private Equity

P.L. 119-21, also called the One Big Beautiful Bill Act or OBBBA (the Act), was signed into law in July 2025, represents one of the most consequential tax overhauls in history. The Act reshapes several incentives that impact the private equity industry — rewarding long-term ownership, capital investment and domestic business expansion.

For sponsors and LPs, the practical effect is clear: there are significant tax benefits available to firms that buy businesses and make qualifying investments with longer holding periods.

"The OBBBA meaningfully reshapes the investment thesis and underlying math for many private equity investors: permanent bonus depreciation, deduction of R&E expenses, broadened Section 1202 qualifications, and relaxed interest expense limitations don’t just enhance returns, they increase incentives to invest in growth and make smaller companies more appealing to private equity.”

Bonus Depreciation and Deduction of R&E Expenses: Immediate Cash Flow From Capital Spending

The Act restored 100% bonus depreciation, allowing businesses to immediately expense qualified equipment, machinery and technology investments. The Act also eliminated the requirement to capitalize domestic research and experimental (R&E) expenses, instead allowing for the current deduction of such eligible expenditures.

For private equity sponsors, eligible investments now create immediate tax deductions rather than delayed benefits. Many founder-owned companies that may have historically underinvested in their businesses now have the incentive to deploy capital to qualified capital expenditures (CapEx) and R&E endeavors, which can help improve after-tax cash flow post-closing and support higher purchase prices on exit.

Strategic Effects

- Greater appetite for platforms in industries with CapEx needs

- Higher anticipated after-tax cash flows

In practice, buying and heavily investing in now produces faster after-tax earnings than simply holding it unchanged.

Section 1202 (QSBS): The Long-duration Incentive

The Act broadened Section 1202 eligibility and gain exclusion limits, allowing investors to exclude a substantial portion — or in some cases all — of capital gains after a qualifying holding period.

This dramatically changes exit incentives. A longer hold can produce materially higher after-tax returns than a quicker sale at a similar valuation.

Observed Industry Responses

- Buyout firms investing earlier in company life cycles

- Enhanced IRR through incremental capital gain exclusions on exit

- Increased utilization of C-corporation holding structures

The provision rewards patient ownership and sustained scaling rather than rapid flipping.

Section 163(j): The Constraint on Financial Engineering

The Act also made taxpayer-favorable changes to the Section 163(j) business interest limitation, increasing the amount of interest expense companies can deduct relative to earnings. For private equity, this further improves the traditional tax advantage of leveraged buyouts.

Consequences

- Reduced equity contributions from sponsors

- Greater after-tax cash flows for debt-funded investments

In effect, the Act did not simply change tax rates — it reoriented incentives. By pairing immediate expensing benefits with long-term capital gains exclusion, the law rewards patient ownership and capital improvements.

For additional information on these and other key provisions of the bill, see Cherry Bekaert’s article: The OBBBA: 8 Key Takeaways for Private Equity Investors, Family Offices, Fund Managers and Their Portfolio Companies.

From Wall Street to Main Street: Private Equity’s Race for Retail and 401(k) Capital

Private equity firms are increasingly targeting individual investors as institutional fundraising slows and demand for private assets broadens. Major managers such as Blackstone, Apollo Global Management and KKR have launched semi-liquid and evergreen funds designed for wealth platforms, lowering minimums and offering periodic liquidity. They are also partnering with retirement recordkeepers like Fidelity Investments and Vanguard to introduce private credit and diversified private market allocations inside managed accounts and 401(k) structures.

Government regulators have signaled a willingness to support this expansion, with the U.S. Department of Labor updating guidance to allow more flexibility for private assets in retirement plans and the U.S. Securities and Exchange Commission considering frameworks that encourage broader retail access while maintaining disclosure and investor protection standards. This convergence of private equity innovation and regulatory openness is opening new avenues for individual investors to participate in previously institutionalonly markets.

Private Equity Industry Outlook: 2026 and Beyond

The private equity industry outlook for 2026 points to a period of renewed momentum following several years of market recalibration. Looking further ahead, the industry is evolving structurally. PE firms are placing greater emphasis on operational value creation, digital transformation and AI-driven efficiencies rather than relying primarily on leverage.

Private credit is becoming a permanent fixture of deal financing, while continuation funds and longer hold periods are increasingly common. Although challenges remain, the overall outlook suggests a more disciplined, sophisticated and resilient PE market entering its next growth phase following a remarkable 2025.

- Increased Deal Activity Expected To Keep Momentum: PE deal volume is forecast to rise in 2026, continuing the rebound that started in 2024, with PE deal activity outpacing overall M&A growth as sponsors gain confidence and valuation gaps narrow.

- Dry Powder Declines, Capital Availability Remains High: Capital availability remains large but is beginning to unwind. PE dry powder declined from record highs in 2024, signaling that funds are actively deploying capital rather than sitting on it. However, the industry still holds substantial uncommitted capital, which continues to support large buyouts and sector roll-ups.

- Exits and Liquidity Levels Evoke Cautious Optimism: After a strong 2025 rebound, exits in 2026 are expected to broaden rather than surge. Activity should remain healthy as sponsors work through a backlog of older investments, led by strategic and sponsor-to-sponsor sales with selective IPOs. While 2025 reopened the market, 2026 looks poised to normalize it.

- Market Structure and Strategic Trends Steer Investor Attention: PE is increasingly concentrating on key growth verticals such as technology (especially AI-related infrastructure), healthcare, financial services and energy infrastructure. AI adoption is influencing both investment targets and internal PE operations, making tech-enabled companies highly sought after.

- Operational Transformation Provides Competitive Advantage: Firms with deep operational expertise are gaining an edge, as buyouts move beyond financial engineering toward real growth and productivity gains within portfolio companies.

- Competition Spurs Consolidation and Creative Dealmaking: Competition from strategic buyers and sovereign wealth funds is intensifying, pushing PE funds to differentiate through value-creation capabilities. The industry may see consolidation among midmarket managers and growth of larger platforms that can handle complex deals.

- Fundraising Headwinds May Hinder Future Portfolios: Fundraising remains below peak levels, especially for traditional funds, which may compress competition for capital and reshape future portfolios.

- Economic and Policy Uncertainty Undermine Investor Trust: Macroeconomic volatility and policy uncertainties (e.g., regulatory changes and geopolitical strife) remain top concerns for deal execution and investor confidence.

- Tax Incentives: Recent tax reform that is generally business-friendly has contributed to a positive outlook for private equity by reshaping incentives to generally improve after-tax cash flows for investors. Middle-market PE firms are also systematically assessing the potential tax benefits of their acquisition structures and related holding periods to maximize after-tax returns on exit. These developments further reinforce expectations of a strong deal market in 2026.