In accordance with 45 CFR Part 75, your government grant funding award comes with rules, regulations and audit requirements. On October 1, 2025, the U.S. Department of Health and Human Services (HHS) phased out 45 CFR Part 75 and migrated to 2 CFR 200 with certain HHS-specific modifications relocated to 2 CFR Part 300. If you receive federal grant funding, this in-depth guide provides the details and tips to avoid trouble and stay compliant.

45 CFR Part 75: Overview of Grant Funding Regulations

Grant funding is frequently thought of as “free money.” While the government oversight of a project funded by a grant is less intrusive than a true contractual relationship with the federal government, there are still rules that need to be adhered to in compliance with 45 CFR Part 75 — including audit oversight.

There are many agencies that fund grants that are subject to Uniform Guidance Audits (UGA), including:

- National Institutes of Health (NIH): Major funding source for biomedical research

- Department of Energy (DOE): Funds energy, science and defense projects

- National Science Foundation (NSF): Supports fundamental research across all scientific fields

- U.S. Department of Agriculture (USDA): Funds food, agriculture and rural development

- Department of Homeland Security (DHS): Grants for security and emergency management

- Department of Transportation (DOT): Aviation (FAA) and transit funding

- Department of Labor (DOL): Workforce development grants

- Environmental Protection Agency (EPA): Environmental research and compliance grants

- Department of Defense (DoD): Army Medical Research Grants (CDMRP)

Because NIH accounts for the majority of federal grant funding subject to Uniform Guidance, we will use NIH as the primary reference point for simplicity. There are two types of audits that these grants, cooperative agreements and similar assistance awards are subject to:

- Uniform Guidance Audits (UGA), also called Single Audits. For the purpose of this article, UGA includes any agency variations of this type of grant audit.

- The annual Incurred Cost Submission. This “true up” report is the primary document used by government auditors to negotiate final grant costs, including indirect costs. The Office of Management and Budget (OMB) offers a deep dive into all the Indirect Cost Submission requirements.

This guide explores UGA requirements, including dollar thresholds and due dates, as well as the most common UGA findings we see in our practice.

One of the key concepts of grantsmanship presumes that grantees act with integrity — to the point of policing themselves. While it is difficult to police yourself when you don’t understand the rules, it is your responsibility to understand them.

Grant Audit Requirements

If an awardee organization has expenditures from grants that exceed $1 million, then it is subject to a UGA. The awardee is required to hire and pay for a certified public accounting (CPA) firm professionally qualified to conduct this type of audit, which encompasses both financial and compliance components.

Once the audit is complete, the awardee submits the audit report to the funding agency, identifying any “findings,” which are violations of laws, regulations or the provisions of the grant. The auditor’s report is reviewed by the Inspector General’s Office (IG) for quality control purposes, and the CPA firm’s work papers may be audited by the IG.

Finally, the funding agency follows up on the findings with the grantee to ensure they have been remedied. Failure to properly respond could result in the agency freezing existing funding.

Regardless of how much funding has been drawn from NIH’s Payment Management System (PMS), you are required to be audited based on expenditures, in accordance with generally accepted accounting principles (GAAP). This includes your reimbursable, allowable costs according to the Federal Acquisition Regulation (FAR).

Whether you are audited or not, you are still required to follow the rules.

Common Uniform Guidance Audit (UGA) Findings

The objective of a UGA is to ensure the recipient of federal funds has not violated any laws, regulations, grant provisions or any of the 12 compliance requirements. It is important to note that any overdraws or overbillings that occur must be repatriated immediately, and funds can be clawed back. Listed below are some of the more common findings.

Issues with Subcontractor Monitoring

Sub-recipients of federal funds are required to comply with the terms and conditions of the prime recipient’s award. Prime recipients that pass funds through to a sub-recipient have a fiduciary responsibility to make sure the subcontract agreement contains the proper legal language that informs the sub-recipient of their obligations. The most common audit findings we see relate to:

- Not properly informing the sub-recipient of their responsibilities under the award

- Prime recipients not properly monitoring sub-recipient’s use of federal funds in compliance with laws, regulations and the provisions of the grant award

- The prime recipient failing to have a documented sub-recipient monitoring policy

Issues With Consultant Documentation

A subcontractor has a clearly defined scope of work on a project. Relationships with consultants are generally less structured. In order for the government to be assured that real work has taken place and that you aren’t just writing a check to a colleague, consultant’s invoices are required to be very detailed and must include a clear description of what grant number they worked on, what they did, when they did it and the hourly rate charged. Additionally, there must be a written consulting agreement.

Improper Allocation of Cost Sharing

Some government agencies require the grantee to share the cost of the research and development effort. This is referred to as cost sharing. Think of this as the grantee and the federal government proportionally sharing in each dollar of a project’s total funding.

As an example, an award may be granted with a 30% cost share. That means the grantee and/or its sub-recipients must fund $0.30 for every $0.70 of government funding towards the $1.00 of total project funding.

Certain types of funding vehicles have mandatory cost-share provisions. As an example, DOE ARPA-E awards typically come with a 10% – 50% cost share requirement embedded in their agreements.

A common audit finding is that grantees don’t properly calculate the amount of their cost share, or the cost share is not applied consistently.

Salaries in Excess of Agency Specific Caps

Most government funding agencies place a limit on the maximum compensation allowed to be charged to their projects. To compete for the best talent, we find grantees unknowingly pay employees in excess of the compensation limits and try to charge the government because they are not aware of the caps on compensation, or don’t know how to properly handle the excess compensation.

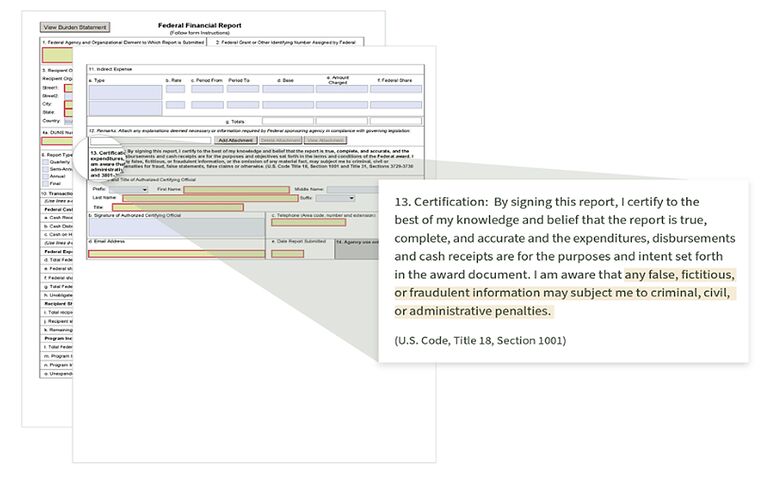

Improperly Filed Federal Financial Form (FFR)

The Federal Financial Report (FFR), also called SF 425, is used to reconcile amounts earned in accordance with the NIH Grants Policy Statement to amounts drawn down from the PMS.

The DOE requires quarterly FFR filings. With NIH, the FFR is required on an annual basis (except for domestic awards under the Streamlined Noncompeting Award Process (SNAP)) and is due within 90 days of the end of your calendar quarter in which the budget period ends. A final FFR also needs to be submitted at the completion of the award agreement within 120 days after the end of the period of performance.

Please note: Similar language is embedded in every PMS drawdown in the fine print. Each time you click ‘Request Payment’, you certify accuracy.

Overdrawing Funds (Overbilling the Government)

As discussed above, grantees are allowed to electronically draw funds from the agencies’ online payment systems. Billing the government, or “drawing down funds,” is as simple as logging in, entering the amount requested, and the funds arrive in your bank account the next business day. Funds should only be drawn down as disbursements are incurred and released to vendors. Drawdowns work on the honor system.

Overdrawing funds is one of the most severe findings, and funding agencies require the immediate repayment of funds. Overdrawing occurs in two common forms: overdrawing for direct costs and overdrawing for indirect costs.

Overdrawing for Direct Costs

Grantees are allowed to draw funds for direct costs incurred (actually spent and released to the vendor), yet we occasionally find grantees drawing funds for costs to be incurred in the future. We also see situations where the grantee draws lump sums of money, say $100,000, to bridge cash shortages even though their actual grant expenses incurred may be much less. This is usually a symptom of having an inadequate indirect cost rate.

Overdrawing for Indirect Costs

This finding is much more common. The government will reimburse grantees for indirect costs, or costs that are not directly related to a specific project, but rather, benefit all projects or the whole company. When a grant is proposed, the grantee includes an indirect cost rate in its proposal to cover such expenses. This “provisional” indirect rate is typically a percentage of direct costs and is a temporary billing rate that must eventually be trued-up to actual expenses.

Sometimes, an indirect cost rate will be negotiated prior to the award being funded. Other times, no negotiation is required, because the agency will approve very low indirect rates with “no questions asked”. For example, NIH SBIR grantees that propose a facilities and administrative (F&A) rate of 40% or less do not have to negotiate their indirect rate — it is accepted as proposed. This can be known as a “safe rate”, but our observance leads us to believe that this can be anything but “safe”.

Inadvertent Fraud

Some grantees may commit “inadvertent fraud” as a result of not monitoring their actual indirect cost rate and not maintaining proper job cost reports on an ongoing basis. The FAR requires indirect costs to ultimately be reported and reimbursed at the lower of actual costs or the capped provisional indirect rate.

Follow the potential trap:

- You receive a grant and think of it as “free money”

- You requested a low provisional indirect cost rate (F&A rate < 40%) in your proposal, so you didn’t have to negotiate your indirect cost rate before your award is funded

- Because you didn’t go through the indirect rate negotiation audit process, it’s not obvious that you are still required to calculate actual indirect rates and adjust your billings at the end of the year

- You establish a billing relationship with the PMS systems whereby you push a button and whatever you requested shows up in your bank account the next day

- When you file the FFR on a quarterly basis, you simply fill in whatever amounts you have drawn as being “earned”

Expenditures must be based on GAAP, including properly maintained job cost reports and indirect rate calculations. Grantees must also consider the FAR, agency supplemental regulations, vehicle funding restrictions, and any cost-sharing language or restrictions placed in each specific grant award.

“Inadvertent fraud” may be committed when signing the certification located on line 13 of the FFR (SF 425).

It is critical to understand that if you don’t negotiate your indirect cost rate, your indirect rate is capped at whatever you proposed. As such, you have forfeited the right to re-budget other spending categories to pay for indirect expenses that exceed this cap.

Your Guide Forward for Managing Your Risk

At Cherry Bekaert, our Government Contractor Consulting Services professionals bring deep knowledge of agencies, regulations and compliance to help you navigate the complexities with confidence. We work alongside you to mitigate risk while aligning with your strategic business objectives.

Our goal is to provide insights that empower you to manage your grant funding effectively and reduce the likelihood of undesired audit findings. If you’d like to explore how we can support your organization, we’re ready to listen and collaborate on solutions tailored to your needs.

Related Insights