On March 12, 2026, Brandon Lord, executive director of the U.S. Customs and Border Protection (CBP)’s trade policy and programs directorate, filed a declaration with the U.S. Court of International Trade (CIT) providing an update that the upgrades to the automated commercial environment (ACE) system are underway. In response, Senior Judge Richard K. Eaton continued his pause of his March 4, 2026 (modified March 5, 2026) order for CBP to immediately begin the refund process.

Background

On March 4, 2026, the CIT decided in favor of the plaintiff in Atmus Filtration, Inc. v. United States, ordering the CBP to immediately begin issuing refunds of the IEEPA tariffs to importer of records. On March 6, 2026, the CBP filed a declaration requesting a 45-day extension for updates to the ACE system to prepare for the massive volume of refund submissions (over $166 billion of tariffs collected from over 330,000 importers of record).

That same day, in response to the CBP declaration, Senior Judge Richard K. Eaton paused his prior order and ordered that CBP provide an update to the Court on March 12, 2026.

Update of CBP’s Progress

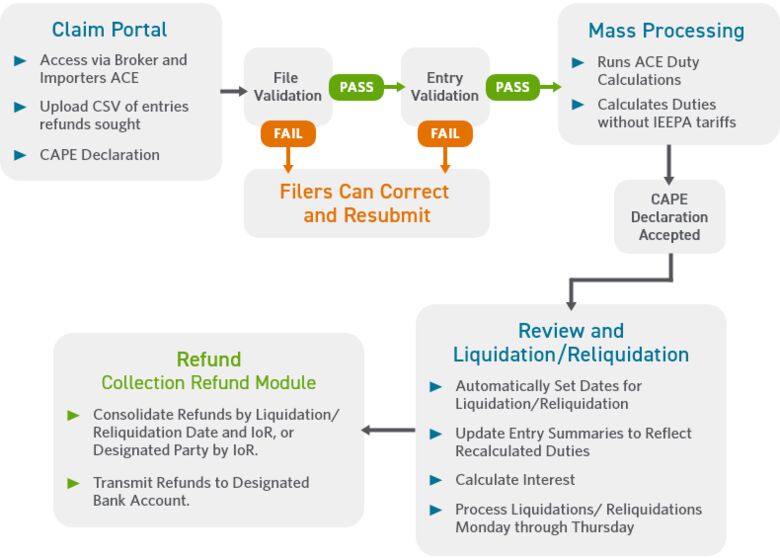

On March 12, 2026, Lord, on behalf of the CBP, filed the mandated update to the Court (Updated Declaration). In the Updated Declaration, the CBP stated the new ACE functionality is named the Consolidated Administrative and Processing Entries (CAPE).

CAPE has four integrated components:

- Claim Portal

- Mass Processing

- Review and Liquidation/Reliquidation

- Refund

The CBP update noted the claim portal component is currently 70% complete, the mass processing component 40% complete, the liquidation/reliquidation component 80% complete, and the refund component 60% complete.

Initial Testing in the Claim Portal

After an importer or broker has uploaded the CSV, or the CAPE Declaration) two validations will be sequentially performed:

- File Validation: This process is intended to confirm that all necessary information was included in the submission, it is properly formatted, the filer is the importer of record (IoR) or the authorized broker, and the file itself is not corrupt. A failure of the File Validation will trigger the ACE system to report the specific error, and filers will be allowed to correct and resubmit on a new CAPE Declaration.

- Entry-specific Validation: The process is intended to confirm entry-specific points, such as confirming the entry submission number exists in ACE and at least one IEEPA Harmonized Tariff Schedule Chapter 99 number was declared on it. Any specific entry that fails this validation will be struck from the CAPE Declaration, but the CAPE Declaration will continue to be processed the remaining entries. Any struck entries can be identified by the filer within ACE and filers will be allowed to correct and resubmit those entries on a new CAPE Declaration.

What is Next

The above breakdown of CAPE is the expected basic functionality the agency is developing to handle IEEPA tariff refund claims. This basic functionality is expected to be sufficient to handle the majority of IEEPA tariff refund claims, except for:

- Unliquidated entries subject to antidumping or countervailing duties,

- Entries with an ACE liquidation status of “suspended,” “extended,” or “under review,” and

- Certain entries such as warehouse withdrawal, drawback claims, etc.

CBP is taking a phased development approach to CAPE. The agency has committed to providing a detailed user-guide on scope and functionality as each phase of development is completed and implemented.

Your Guide Forward

Cherry Bekaert’s International Tax and Tax Policy teams will continue to provide updates on the IEEPA tariff refunds as development occurs. Reach out to an advisor today for any questions you have while navigating these rapid changes.

Related Insights