Alternative investments are being reshaped by a convergence of powerful, cross-asset trends. “Higher-for-longer" interest rates and tighter liquidity are redefining underwriting standards, capital structures and return expectations across private equity, private credit, hedge funds and real assets.

At the same time, fundraising dynamics have become more selective, with institutional allocators consolidating manager relationships and prioritizing scale, track record, and differentiated strategies. Technological implementation, particularly artificial intelligence (AI) and data analytics, is transforming sourcing, transparency and portfolio value creation but not without introducing new operational and cybersecurity risks.

Regulatory scrutiny continues to rise, influencing everything from valuation practices to investor reporting. The growing emphasis on operational value creation, resilience and sector specialization is driving managers to move beyond financial engineering toward more hands-on, thesis-driven investment approaches.

This Alternative Investments Brief explores some of the key trends observed across alternatives in 2025 and the emerging themes taking hold so far in 2026.

Technology: Artificial Intelligence Dominates Headlines

AI has rapidly evolved from a thematic consideration into a central pillar of capital deployment and value creation across the alternatives landscape. Private equity (PE) firms are aggressively pursuing platform investments in AI-native companies while also backing traditional businesses with clear pathways for AI-enabled transformation. Venture capital remains heavily concentrated in foundational models, infrastructure and applied AI solutions, while growth equity is funding the scaling of commercially proven platforms. Beyond direct investments, managers across private equity, private credit and real assets are embedding AI into their own operations to enhance deal sourcing, underwriting, portfolio monitoring, and exit timing.

At the same time, the implementation of AI is intersecting with several adjacent investment themes. The buildout of digital infrastructure, including data centers, cloud capacity, and semiconductor supply chains, is attracting significant capital across private markets and real assets strategies. In private credit, lenders are increasingly financing AI-driven companies and structuring bespoke capital solutions tied to high-growth, asset-light business models. The rise of AI is accelerating the demand for energy and power solutions, particularly in renewable and transitional energy assets, creating opportunities at the intersection of technology and infrastructure. As competition for differentiated deals intensifies, firms that can combine domain expertise, proprietary data and AI capabilities are increasingly positioned to outperform.

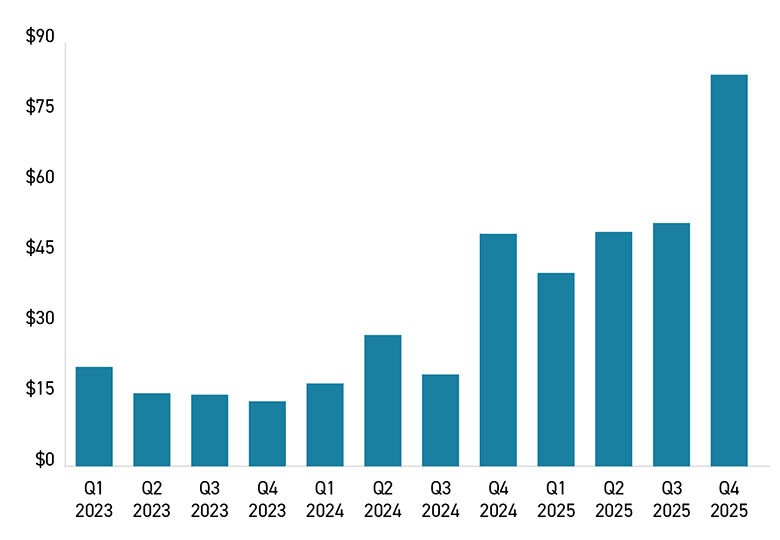

Global Equity Funding Behind the AI Revolution ($U.S. Billions)

Source: CB Insights | State of AI Global 2025 Recap

As of January 2026

Despite the recent increase in capital investments, this past year may very well have marked the end of a critical phase in artificial intelligence. AI technology is expected to move away from its funding phase into a phase of implementation and real-world results. The next year could prove critical to AI and its ultimate success. AI adoption and implementation will most certainly have downstream effects on the general stability of global financial markets, given the incredible investments thus far, be those positive or negative.

Geopolitics: U.S. Trade Policy Ignites Volatility

Geopolitical developments in recent months have become a more immediate and disruptive force across alternatives, with U.S. trade policy at the center of this shift. A renewed emphasis on tariffs, export controls and industrial policy, particularly in strategic sectors such as technology, energy and critical minerals, has introduced sharper market reactions and episodic volatility across both public and private markets. These policies have accelerated supply chain realignment toward domestic production but have also increased input costs, compressed margins, and complicated cross-border dealmaking. As a result, asset managers are placing greater weight on geopolitical risk pricing, jurisdictional exposure and downside protection in underwriting.

The direct fallout has been especially pronounced in energy markets, where geopolitical tensions and policy shifts have contributed to heightened price swings in oil and gas. Supply disruptions tied to ongoing global conflicts, combined with evolving U.S. tariff and energy policies, have created a more reactive and sentiment-driven commodity environment. Organizations such as the Organization of the Petroleum Exporting Countries (OPEC) continue to influence supply dynamics, but policy uncertainty and shifting global demand expectations have amplified volatility.

For investors, this has translated into both opportunity and risk: strong near-term cash flows and attractive entry points in traditional energy assets, alongside increased difficulty in forecasting long-term pricing and exit environments. More broadly, the persistence of policy-driven volatility is pushing alternative managers to adopt shorter underwriting horizons, dynamic hedging strategies, and more flexible capital structures to navigate an increasingly fragmented and unpredictable global market.

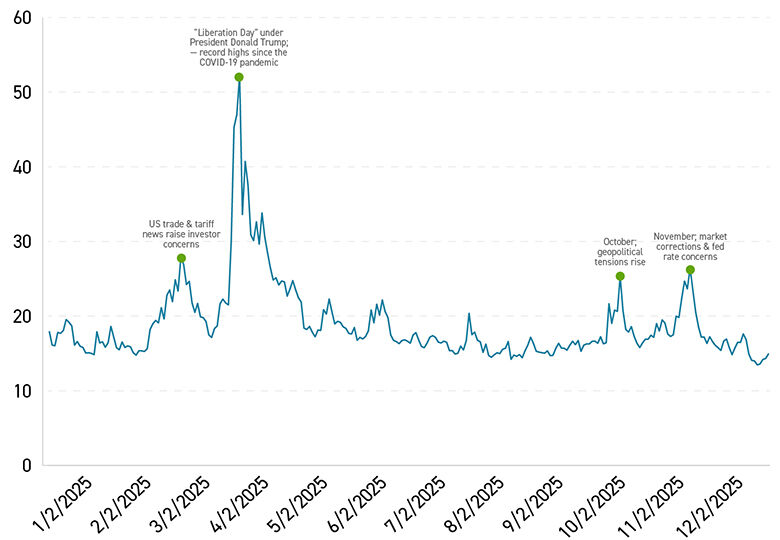

2025 Daily CBOE Volatility Index (VIX)

Source: Cboe Global Markets | Historical index data

As of January 2026

Macroeconomics: Improving Conditions Stir Cautious Optimism

While broader economic realities continue to influence the alternative investment market, the environment has begun to shift following interest rate reductions by the Federal Reserve in late 2025. After an extended “higher-for-longer” period, the initial easing cycle has provided some relief to financing markets, lowering the cost of capital and improving debt availability across private equity, private credit, and real assets. While rates remain elevated relative to the prior decade, the directional change has begun to stabilize deal activity, narrow bid-ask spreads, and support a gradual recovery in transaction volumes. At the same time, investors remain cautious, as inflationary pressures and policy uncertainty continue to temper expectations around the pace and durability of further cuts.

These evolving macro dynamics are also creating more nuanced and, in some cases, destabilizing effects across capital formation and liquidity. While improved financing conditions have modestly supported exit pathways, private credit markets are facing emerging “run risk” dynamics, as a subset of investors reassess liquidity in semi-liquid and open-ended structures. Heightened sensitivity to credit performance, coupled with tighter spreads and increased competition, has prompted more selective capital allocation and, in some cases, redemption pressure. This has introduced a greater focus on liquidity management, asset quality and structural protections within credit vehicles. More broadly, alternative managers are recalibrating underwriting assumptions to reflect a more fragile equilibrium, balancing improving macro tailwinds with pockets of liquidity risk, and reinforcing an emphasis on downside protection, disciplined deployment and portfolio resilience.

Regulatory: Agencies Poised To Act

Government regulation has become an increasingly influential force across the alternative investment landscape, particularly as policymakers respond to market evolution, systemic risk concerns, and the rapid growth of private markets. Heightened scrutiny from the U.S. Securities and Exchange Commission (SEC) has driven increased transparency, reporting requirements, and governance expectations for private equity and private credit managers. Recent rulemaking and enforcement trends have focused on areas such as fee disclosures, valuation practices, and conflicts of interest, raising compliance costs while also reshaping how firms structure funds and communicate with investors. At the same time, banking regulation has had second-order effects, as tighter capital requirements on traditional lenders continue to shift more financing activity into private credit markets.

Looking Ahead

The regulatory environment remains fluid, with potential policy shifts tied to election cycles, evolving antitrust enforcement, and increased oversight of systemically relevant non-bank financial institutions. For private credit, growing concerns around leverage, liquidity mismatch, and “run risk” in semi-liquid structures are drawing closer attention from both the SEC and the Financial Stability Oversight Council. This has introduced the possibility of enhanced disclosure standards, stress testing expectations and broader systemic risk frameworks. Across asset classes, managers continue to adapt by institutionalizing compliance functions, embedding regulatory considerations into fund design and underwriting, and proactively engaging with policymakers. In this environment, regulatory agility and operational sophistication are critical differentiators as firms navigate a landscape where oversight continues to evolve in step with alternative assets.