Corporate treasury is undergoing a rapid transformation, extending beyond cash to increasingly include digital assets. The rise of digital asset treasury companies (DATCOs) — a new class of public companies that integrate digital assets into their primary business operations and balance sheets — is reshaping capital strategy, drawing attention to accounting innovation and operational infrastructure.

These capital strategies are no longer confined to niche innovators, and, as they enter the mainstream, DATCOs face a complex intersection of financial reporting, process modernization and cybersecurity risk.

What Is Corporate Treasury?

Corporate treasury focuses on managing financial risks and ensuring an organization maintains adequate liquidity to meet its obligations. Traditionally part of the accounting department, corporate treasury has evolved into a distinct discipline responsible for overseeing risks related to interest rates, credit, currency fluctuations and operational controls.

Corporate treasury is critical to safeguarding company value and supporting strategic financial decisions, often reporting directly to the CFO or serving on executive leadership teams. Therefore, treasurers will develop board-approved policies to manage these risks and often work closely with internal and external financial professionals, including auditors, bankers and consultants.

What Is a Digital Asset Treasury Company (DATCO)?

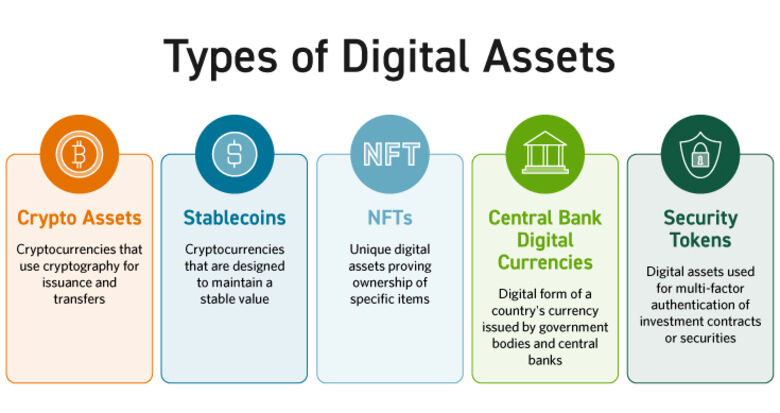

A digital asset treasury company (often called a DAT company or DATCO) is a publicly listed firm whose primary purpose is to own and manage digital assets directly on its balance sheet. Digital assets include crypto assets or cryptocurrencies (e.g., bitcoin ), tokenized securities, stablecoins and non-fungible tokens (NFTs), among others.

In these companies, the treasury function is not a supporting activity but the core of the business itself. The company raises capital through traditional equity and debt markets and allocates that capital into digital assets, treating them as long-term strategic reserves rather than incidental investments. Investors gain exposure by purchasing shares of the company, effectively accessing crypto markets through familiar equity instruments instead of holding the assets directly.

DATCOs provide a simple, regulated pathway to digital asset exposure within brokerage accounts, retirement plans and institutional portfolios. Beyond access, they aim to create value through active balance‑sheet management using capital markets, financing strategies, custody infrastructure and disciplined risk management to grow their digital asset holdings over time.

Unlike passive vehicles that merely track the price of a cryptocurrency, a well‑run DATCO seeks to outperform the underlying asset by compounding holdings per share and leveraging management expertise to turn digital assets into a scalable corporate strategy.

Traditional Corporate Treasury vs. Digital Asset Treasury

Corporate treasuries manage traditional assets, such as cash, bank deposits and marketable securities, while DATCOs manage digital assets. DATCOs represent a new frontier in corporate finance, offering opportunities for diversification and alignment with broader market trends. However, digital assets also introduce volatility, structural complexity and cyber risk that must be addressed specifically and proactively.

The following comparison table outlines the primary differences between corporate treasury and digital asset treasury:

| Corporate Treasury | Digital Asset Treasury | |

|

Primary Assets |

Cash, bank deposits, bonds, equities | Cryptocurrencies, stablecoins, tokens |

|

Risk Management |

Interest rate, credit, FX, liquidity | Cybersecurity, market volatility, regulatory, custody |

|

Processes |

Bank transfers, wires, cash pooling | Blockchain transactions, wallet management, smart contracts |

|

Infrastructure |

ERP, TMS, banking platforms | Wallets, custodians, blockchain integrations |

|

Controls |

Dual approvals, reconciliations, audits | Multi-signature wallets, key ceremonies, API security, blockchain audit trails |

|

Reporting |

Standard financial statements, cash flow | Crypto asset accounting, on-chain/off-chain reconciliation |

|

Regulatory |

Established frameworks (GAAP, IFRS, SOX) | Evolving standards (ASU 2023-08, SEC guidance, global crypto regulations) |

|

Talent Needs |

Finance, accounting, banking expertise | Blockchain, cybersecurity, digital asset compliance expertise |

The History of DAT Companies

The origins of the modern digital asset treasury company can be traced back to 2020, when Michael Saylor led MicroStrategy (now known as Strategy) in a highly visible shift to adopt bitcoin as a core corporate treasury asset. What began as a tactical response to inflation risk evolved into a defining balance sheet strategy, reframing digital assets as long term reserves rather than speculative holdings. By pairing sustained asset accumulation with capital markets activity, Strategy demonstrated that public companies could use traditional equity and debt financing to systematically scale digital asset exposure, laying the conceptual foundation for the DATCO model.

For several years, this approach remained largely confined to a small number of early adopters. Its broader adoption accelerated as market infrastructure and regulatory clarity improved, culminating in a critical accounting milestone: ASU 2023-08, Accounting for and Disclosure of Crypto Assets, which was long sought by the industry after years of applying the impairment‑only model under ASC 350-60.

The new standard marked a meaningful shift toward accounting frameworks that better reflect the economic reality of digital assets, enabling in‑scope digital assets to be measured at fair value (FV) with enhanced disclosure and bringing much‑needed consistency, transparency, and credibility to how these assets are presented in corporate financial statements for investors, boards and regulators.

Together with strengthening crypto markets and growing institutional participation, these developments transformed digital asset treasury management from an experimental strategy into a repeatable corporate model. What began as a single company’s balance‑sheet decision had expanded from fewer than 10 DATCOs in 2021 to roughly 200 today, according to DLA Piper.

Strategies for Operating a Digital Asset Treasury Company

For DATCOs — where the balance sheet itself is the business — operating at scale demands modern digital asset accounting systems, proactive risk management, and strong safeguards around asset movement, system integrations and third‑party exposure.

Modernizing Accounting Systems for Digital Assets

Digital asset adoption necessitates the financial transformation of corporate accounting functions through the modernization of and integration with existing finance systems. Treasury management systems, enterprise resource planning (ERP) platforms and existing intercompany processes must be able to accommodate digital asset wallet activity, new custodial arrangements, and potentially even yield mechanisms.

A holistic finance modernization effort should include process, compliance, controls, and reporting across finance and accounting functions.

Managing Digital Asset Marketplace Risk and Corporate Structure Fragility

The market opportunity for DATCOs is accompanied by inherent systemic risks. Companies that are building around this strategy often rely on stock premiums and access to capital markets to manage their financial risks. However, if sentiment shifts or digital asset market value drops, these frameworks and structures can become hyper-delicate. Corporate leaders need to be considerate of this fragility and should incorporate robust scenario planning to account for this additional risk.

In addition, debt maturities tied to these digital asset strategies may create refinancing pressure, particularly in a volatile pricing environment. Treasury teams and CFOs must model outcomes under various liquidity and market stress scenarios for resilience.

Protecting Against Cyber and Operational DATCO Risk

Digital assets introduce new opportunities for cyber risk, including theft and fraud, as well as other operational breakdowns. To mitigate these risks, DATCOs must design and implement governance frameworks that define roles, approvals, custody models and audit trails, focusing on three main focus areas: the movement of funds, integrations and due diligence.

Controlled Movement of Funds

Protecting digital assets from cyber and operational risks begins with a simple yet effective good cyber hygiene practice: The controlled movement of funds. The DATCO should enforce segregation of duties supported by quorum approvals and (where applicable) hardware-backed keys. This includes:

- Requiring auditable evidence for every step (approval logs, key-ceremony records, policy-change history).

- Running periodic access reviews.

- Maintaining clearly defined, tested break-glass procedures with post-event oversight.

In practice, this means that digital asset movement follows the same controlled workflow expected for wire transfers.

Integrations and API Security

Most DATCO breaches ride through integrations, not cryptography. Key practices to safeguard against breaches include:

- Locking down the DATCO to ERP/TMS connection.

- Grant least privilege, task-specific scopes.

- Using dedicated service accounts and preferring short-lived “just-in-time” tokens over static keys.

- Adding IP allowlists, mutual TLS (both sides authenticate with certificates), payload signing and monitoring for API configuration drift.

- Finance should be able to see: an API access inventory, key/token-rotation cadence, and a recurring joint review with IT of failed/blocked call logs to prove controls are designed and operating.

Third-party/DATCO Due Diligence

When DATCOs engage third-party providers, such as custodians, cloud service providers and other technology vendors, it’s essential they partner only with organizations that can demonstrate evidence of trust, not marketing — meaning they can demonstrate robust security, operational resilience and transparency. Look for third-party providers that have:

- SOC 1 Type II over transaction processing (and SOC 2 for security).

- Transparency on hardware security module (HSM) and multi-party computation (MPC) design.

- Code-signed policy changes to ensure the platform accepts policy/rule updates only when digitally signed by authorized roles.

- Insider-threat controls in place to ensure segregation of duties, monitoring and activity reviews.

DATCOs should also require visibility into tested recovery time objective (RTO) and recovery point objective (RPO) (how much data can be lost) for cold-storage scenarios, vendor-concentration limits, and a rehearsed, documented exit plan proving you can migrate assets without the provider. These translate directly into audit readiness and operational continuity.

CFO Considerations for Digital Asset Treasury Integration

Finance leaders who approach this space with disciplined governance, modernized infrastructure, and robust risk management will be best positioned to harness and capitalize on this recent innovation and strategy. CFOs should take a structured approach with the following considerations:

- Define the Role of Digital Assets: Understand the purpose and use of the various tokens used in your treasury strategy.

- Strengthen Accounting and Tax Readiness: Integrate required infrastructure and prepare for reporting, model volatility, and anticipate tax implications.

- Build Governance and Cyber Controls: Establish clear custody policies, segregation of duties and audit trails.

- Modernize Treasury and Accounting Functions: Integrate digital asset activity into treasury systems and add additional subledgers to accommodate the new asset class.

- Plan Capital and Liquidity: Leaders need to balance equity, debt and operational reserves to avoid overreliance on market and stock premiums.

- Conduct Continuous Risk Monitoring: Limit access and run access reviews.

- Communicate Transparently: Ensure boards, investors and stakeholders are informed on exposures, governance and strategy.

How Cherry Bekaert Can Help

Cherry Bekaert’s CFO Advisory practice supports clients in restructuring and modernizing their accounting processes to adapt to and support the introduction of digital assets into their treasury strategy. Our team can help integrate these assets into financial reporting systems, providing a clear view of operational and treasury impacts. This includes crafting policies and internal controls for crypto asset holdings, managing liquidity risk and structuring balance sheet exposure.

Related Insights

- Article: What Is the GENIUS Act of 2025? A New Era for Digital Finance

- Webinar: New Crypto Assets Accounting and Disclosure Requirements: Understanding and Implementing ASU 2023-08

- Article: Cryptocurrency Market Trends for 2025: Updates and Industry Insights

- Article: Defense in Depth Is Key To Protecting Your Digital Assets