For emerging government contractors, especially those preparing to bid on cost-type work, an accounting system is more than a back-office function. It is a critical capability the government will evaluate before award and continue to scrutinize after performance begins.

Two types of audits create the most confusion for emerging contractors:

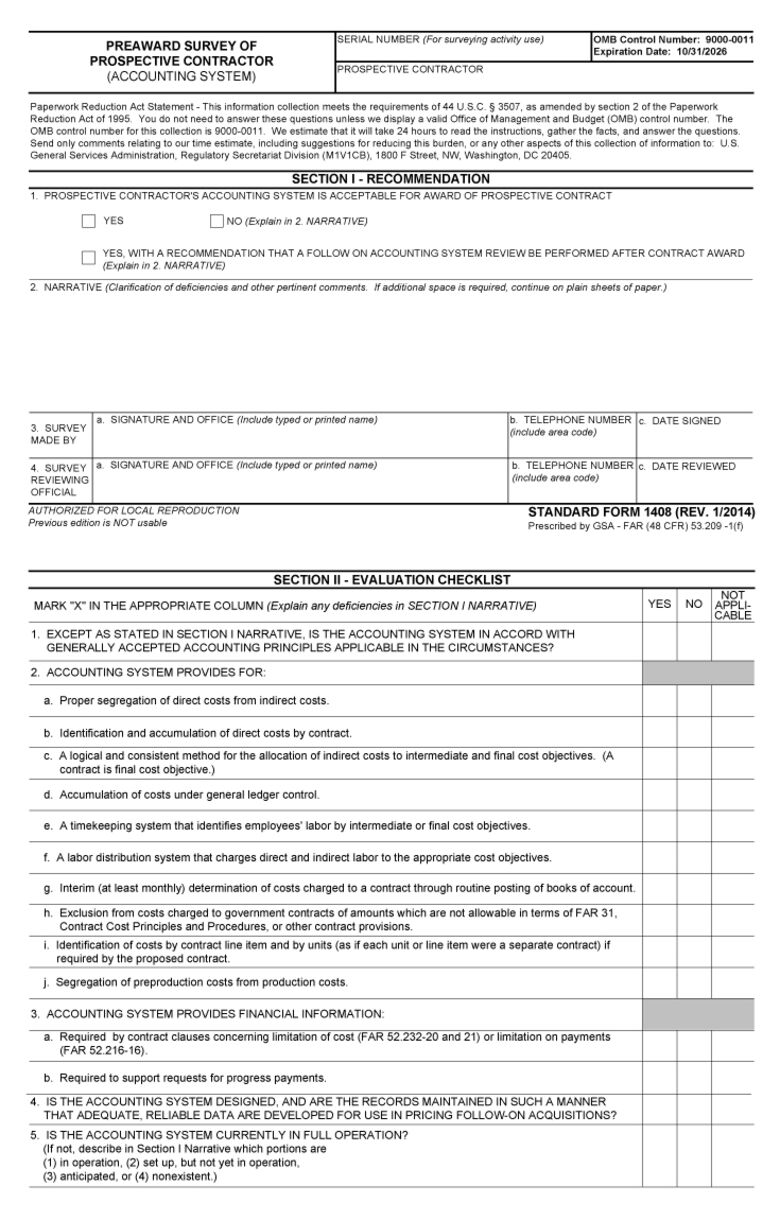

- Standard Form 1408 (SF 1408) pre-award accounting system audit

- Post-award accounting system audit conducted after contract award

While both examine similar fundamentals (e.g., labor tracking, cost segregation, indirect allocation and auditability), they serve different purposes and require different preparation strategies.

A practical way to think about the lifecycle is this: SF 1408 and the pre-award review evaluate readiness, while post-award audits evaluate reliability — whether the system is designed to operate correctly from day one and whether it actually does operate correctly under real contract conditions.

SF 1408 Criteria: Purpose, Requirements and What the Government Is Looking For

What Is SF 1408 and Why Does It Matter?

When a prospective contractor submits a proposal to the Department of Defense (DoD), they are often asked to complete and submit the SF 1408, a pre-award accounting system survey. The SF 1408 is used to document accounting system adequacy and functions as a self-certification that discloses the contractor’s accounting practices for government review.

At a high level, the government wants contractors and subcontractors to be good stewards of federal funds and achieve cost objectives. For DoD work, especially when a cost-reimbursement contract may be awarded, contractors are expected to maintain an accounting system compliant with Federal Acquisition Regulation (FAR) Part 31 (48 CFR Part 31) and aligned with Defense Federal Acquisition Regulation Supplement (DFARS) expectations.

Core Capabilities Reflected in SF 1408

To successfully meet SF 1408 criteria and position your organization for a DoD award, the survey centers on whether your accounting system is in place and can meet DoD’s contract accounting expectations. Key capabilities (as noted in the Section II – Evaluation Checklist screenshot below) include:

- Maintaining a general ledger based on accrual accounting

- Accurately identifying direct costs

- Accurately identifying and allocating indirect costs and fringe benefits

- Segregating unallowable costs (and excluding them from billings)

- Having a written, practiced, demonstrable timekeeping policy with controlled corrections

- Showing distribution of labor costs among accounts and jobs

- Issuing indirect rate and job cost reports periodically and on demand (and reconciling reports to the general ledger)

- Demonstrating understanding of request for proposal (RFP) requirements and the ability to achieve appropriate cost objectives

If gaps exist, the SF 1408 process contemplates that you provide a detailed plan with implementation dates for bringing the system into compliance.

How SF 1408 Connects to the Pre-award Review

Once completed, the SF 1408 is returned to the prospective contracting officer, who typically forwards it to the Defense Contract Audit Agency (DCAA) and requests an initial Accounting System Review.

Pre-award Audits: Timing, Objectives, Readiness and Typical Issues

Why the Pre-award Review Exists

The SF 1408 pre-award accounting system audit exists to protect the government before awarding a cost-type contract. At this stage, no costs have been incurred, and no invoices have been paid; the government is making a forward-looking decision about whether the contractor can properly accumulate, segregate and support costs from day one.

This review is common when a contractor is bidding on a first cost-reimbursable, time-and-materials, or labor-hour contract, or when transitioning from historically fixed-price work into cost-type contracting.

Who Is Involved and What Does Each Party Need?

In a pre-award SF 1408 review:

- The contracting officer seeks confidence that an award will not create downstream billing or audit problems.

- The auditor functions as a gatekeeper, assessing whether the system is adequate to support cost-type work.

- The contractor is often early in government contracting maturity and formalizing processes.

Importantly, the auditor is not necessarily looking for a perfect, fully mature system; they are evaluating whether the system is adequately designed, logical and defensible, as well as whether the contractor demonstrates a clear understanding of what an “adequate accounting system” requires.

What Auditors Ask and What They’re Really Testing

Pre-award SF 1408 interviews focus on how costs flow through your system. Typical questions include how employees record time, how you distinguish between direct and indirect costs, how costs are tracked by contract, how unallowable costs are identified and how you would prepare a cost-type invoice.

What the auditor is really evaluating is coherence: do your answers align with system setup, documentation and reports? Inconsistent answers, even when the system is technically capable, can quickly undermine credibility during a pre-award review.

What Is Actually Tested in Pre-award

SF 1408 pre-award task work is typically design-focused and limited in scope. Auditors commonly review:

- Chart of accounts and job costing structure

- Ability to segregate direct costs by contract

- Logic used to accumulate and allocate indirect costs

- Timekeeping controls and correction procedures

- Job cost reports and reconciliation to the general ledger

- Method for excluding unallowable costs from billings

The emphasis is on capability, whether the system is ready to operate correctly immediately upon award, rather than historical performance.

Why “Low Risk” Matters

For smaller or newer contractors, a key objective is being categorized as “low risk.” Passing the initial accounting system review without findings is therefore critical.

Post-award Audits: What’s Reviewed After Award and Why It Matters

Why Post-award Audits Are Different

Once an award occurs and performance begins, the government’s risk profile changes — costs are being incurred, invoices submitted and taxpayer dollars reimbursed. Post-award accounting system audits answer a different question than pre-award: is the system operating effectively, consistently and reliably under real performance conditions?

At this stage, the government is no longer evaluating intent or readiness; it’s evaluating execution.

How Roles and Expectations Shift

In post-award audits:

- The auditor acts as a verifier, assessing compliance and internal control effectiveness.

- The contracting officer may use audit results to require corrective actions or increase oversight.

- The contractor is expected to demonstrate accountability for actual billing outcomes.

Passing a pre-award audit does not insulate a contractor from post-award findings; weaknesses that may have been invisible at pre-award often surface once transaction volume, invoicing activity and recurring reconciliations become routine requirements.

From “Process Talk” to Evidence Validation

Post-award walkthroughs tend to be more pointed and evidence driven. Auditors may ask to see:

- How timekeeping corrections are approved and documented

- How job costs are reconciled to the general ledger monthly

- Who reviews indirect rate calculations and how often

- How billed costs tie to recorded costs

- How invoice line items trace to source documentation

Here, auditors test whether written policies are actually followed. Any gap between what management describes and what records show typically draws attention.

Transaction Testing and Audit Trails

Post-award audit work is more extensive and operational. Auditors commonly perform:

- Transaction sampling (labor, travel, other direct costs, subcontract costs)

- Reconciliation testing between job cost and the general ledger

- Review of timekeeping corrections and approval evidence

- Evaluation of indirect rate calculations over time

- Verification of audit trails and documentation sufficiency

This is often where informal practices become liabilities, as controls that exist only “in theory” generally do not withstand post-award testing.

Potential Ramifications of Findings After Award

If a contractor cannot demonstrate it is maintaining a compliant accounting system, the consequences can be significant. Pre-award, this may result in denial of a contract or delays until issues are resolved. Post-award, audit issues can lead to recommendations that progress payments be shut off, effectively suspending the contract and impacting cash flow until problems are corrected. Findings can also affect risk classification, potentially resulting in increased scrutiny and additional audits.

How SF 1408, Pre-award and Post-award Audits Connect Across the Contract Lifecycle

Although the SF 1408 pre-award audit and post-award accounting system audits evaluate many of the same fundamental building blocks, they do so with different intent and depth. Pre-award emphasizes whether the system is ready — designed to handle compliant cost accumulation, segregation and reporting. Post-award emphasizes whether the system is working — producing consistent, reconciled, evidence-supported results while the contract is being executed and billed.

SF 1408 vs. Post‑award Audits in Practical Terms

|

Audit Stage |

Primary Focus |

What Is Being Evaluated |

Common Issues Identified |

| SF 1408/Pre-award | Readiness | System structure, documented policies, and the ability to generate compliant cost and financial reports | Structural gaps, such as missing foundational elements or incomplete system design |

| Post-award | Execution | Consistency of application, reconciliations and evidence that controls are operating as designed | Discipline gaps, where established controls are not followed consistently |

Key Takeaways for Government Contractors: Practical Readiness and Ongoing Compliance

Preparing for an SF 1408/Pre-award Review

For emerging contractors, pre-award success is often about simplicity and clarity — having a defensible structure and the ability to explain it consistently. Key preparation areas include:

- A chart of accounts that clearly separates direct, indirect and unallowable costs

- Job costing by contract

- A documented timekeeping policy requiring employee-entered time, supervisory approval and controlled corrections

- A logical (even if simple) indirect rate structure

- Job cost reporting that reconciles to the general ledger

- Written policies and procedures that align with actual or expected

An expensive system is not the requirement; a coherent, well-designed and explainable structure is.

Preparing for Post-award Audits

Post-award readiness is less about assembling documentation at the last minute and more about establishing a steady operational rhythm from contract start. Regular reconciliations, ongoing oversight, routine adherence to policies and retained audit trails create an environment where documentation reflects actual practice.

Operational focus areas include:

- Monthly reconciliations between job cost, general ledger and billings

- Controlled labor correction processes with documented approvals

- Standardized billing support packages

- Consistent indirect rate calculations and periodic review

- Clear ownership for reviews and approvals

- Retention of audit trails as part of normal operations

The goal is to make audit readiness a byproduct of how the business is run, not a special project.

Practical Illustrations (From Real-world Scenarios)

Pre-award readiness gap: A professional services firm believed it was ready for its first cost-type bid because it had accounting software. In practice, costs were tracked by department, time was captured informally, indirect costs were mixed with direct expenses, and unallowable costs were not identified.

We implemented job costing by contract, formalized timekeeping controls, mapped direct and indirect costs, and created simple but effective policies and procedures. The result was enhanced clarity without added complexity. The firm became cost‑type ready without unnecessarily complicating its system.

Post-award control breakdown: A growing contractor that passed its pre-award review struggled as volume increased. Job cost reports were not reconciled monthly, timesheet corrections lacked documentation, billing was prepared outside the accounting system, and indirect rates fluctuated without explanation.

We implemented a monthly close cadence, tightened labor controls, standardized the billing process and stabilized indirect rate calculations. Audit risk decreased, and management regained confidence in its numbers. The system had always been capable. The discipline was missing.

Treat Accounting Discipline as a Lifecycle Requirement

SF 1408 and the pre-award accounting system review help the government determine whether a contractor’s system is designed and ready for cost-type contracting. Post-award audits assess whether that same system operates consistently, reliably and with supporting evidence once performance and billing are underway.

Together, these reviews underscore a single message: contractors that build a coherent structure early and maintain disciplined execution during performance are better positioned to protect cash flow, reduce audit risk and sustain credibility with government customers.

Your Guide Forward

You do not have to navigate this process alone. Whether you are assessing readiness, refining your systems, or responding to audit feedback, experienced guidance can help you focus on what matters most and avoid costly missteps.

Cherry Bekaert’s Government Contractor Consulting team can help you navigate complex compliance requirements and maximize the value of your awards. With a proven track record in government contracts and grants, our professionals provide the guidance you need to avoid costly surprises and stay audit ready.