If you are preparing a National Institutes of Health (NIH) Small Business Innovation Research (SBIR) Phase II cost proposal, calculating an appropriate indirect cost rate is critical to your financial solvency.

Cherry Bekaert provides an Excel-based indirect cost rate projection template with three dedicated tabs for:

- Labor input

- Cost input

- Indirect rate calculation output

Many organizations — particularly those with limited proposal history — aim to keep indirect rates as low as possible to remain competitive, even when they do not yet have a clear benchmark for what those rates should be; however, this template allows you to model assumptions and evaluate how changes impact the final indirect rate.

To help simplify this process, we will walk you through a practical example of how an indirect cost rate (a fringe and facilities and administrative (F&A) rate) is developed and how key assumptions affect the outcome.

The Three-tab Approach To Project an Indirect Cost Rate: An Example

Most proposal writers approach their cost proposal with a focus on keeping fringe and F&A rates as low as possible. Without prior proposal experience linked to fundable priority scores or meaningful feedback from reviewers, most aim to maximize direct billable time in an effort to remain competitive.

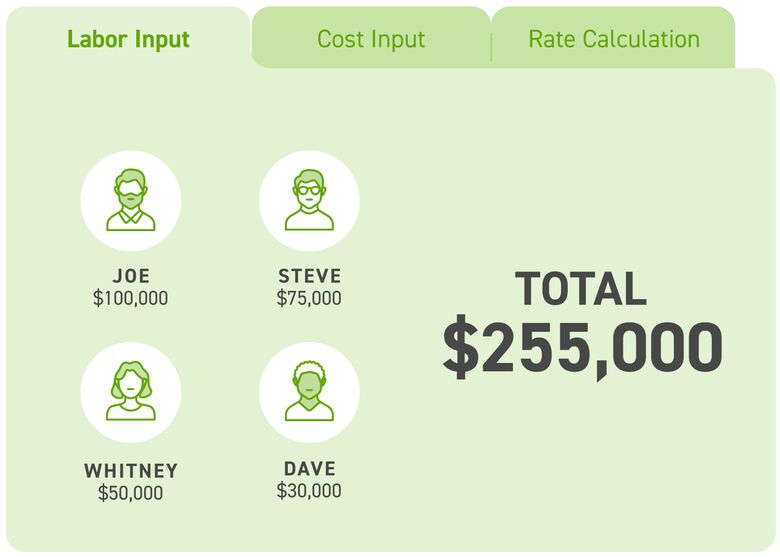

Tab 1: Labor Input for an Indirect Cost Rate Projection

The first tab in our indirect rate projection template focuses on labor inputs — how your people will charge their time. In this simple example, the principal investigator, Joe, plans to pay himself $100,000 a year upon award, reflecting on what he considers a reasonable market-based salary. A critical employee, Steve, will make $75,000 a year, while technicians, Whitney and Dave, will make $50,000 and $30,000 a year, respectively.

Tab 2: Costs Input for an Indirect Cost Rate Projection

In our template, payroll taxes are automatically calculated in the second tab, followed by four other cost categories or sections that you will need to add inputs for. These include:

- Fringe benefits

- Indirect expenses

- Direct expenses

- Unallowable expenses

The top section is fringe benefits, which generally consist of expenses that would not exist without employees. Some fringe benefit examples include workers’ compensation, health insurance, dental insurance, pension plans and disability insurance.

The next section includes indirect expenses. In this example, let’s estimate the following expenses:

- $5,000/year for legal fees

- $10,000 for office and computer supplies

- $600/month for telephone and telecommunication equipment

- $3,000/month for office rent

- $2,500/month for accounting and bookkeeping

The next section includes all the direct expenses for the project, such as materials, consultants, subcontractors and equipment.

Lastly, the fourth section is the unallowable expenses, which must be excluded from the indirect rate cost calculation.

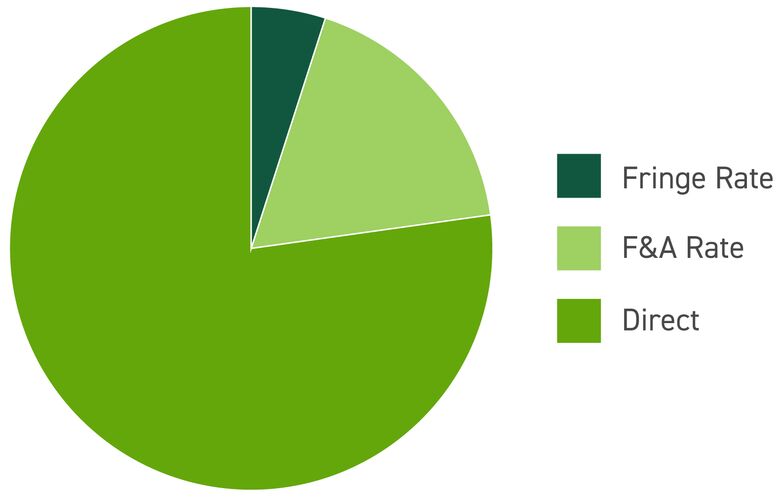

In this first example, 100% of all the labor costs are charged to direct labor and none to indirect labor. As a result, you see a 12.9% fringe benefit rate and a 29.88% F&A rate.

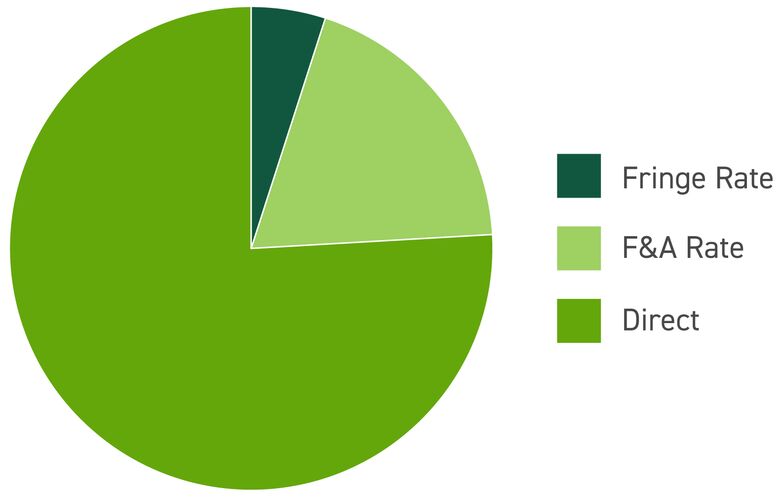

But what happens when that preferred office space isn’t available and the next-best option is $500/month more? The resulting indirect rate will increase a percent or so — not meaningful at all.

This type of change typically does not have a large impact on the overall rate. Indirect cost rates are more strongly influenced by how employees charge their time.

Charging Indirect Labor vs. Direct Labor Has an Immense Impact on Your Indirect Cost Rate

Employees typically don’t work 100% direct on a project. Between vacation, holiday and sick paid time off, almost 10% of their total compensation paid is fringe benefit time (two weeks of vacation, 10 holidays and five vacation days equate to 200 hours out of ~ 2,000 in a year).

Working “In” vs. “On” the Business

As you think about how you want to spend your time, you will most likely want to spend a significant amount of time working “on” the business, rather than working “in” it — shifting a portion of your effort away from direct project work toward business development activities, such as building strategic alliances, diversifying revenue streams and supporting future growth.

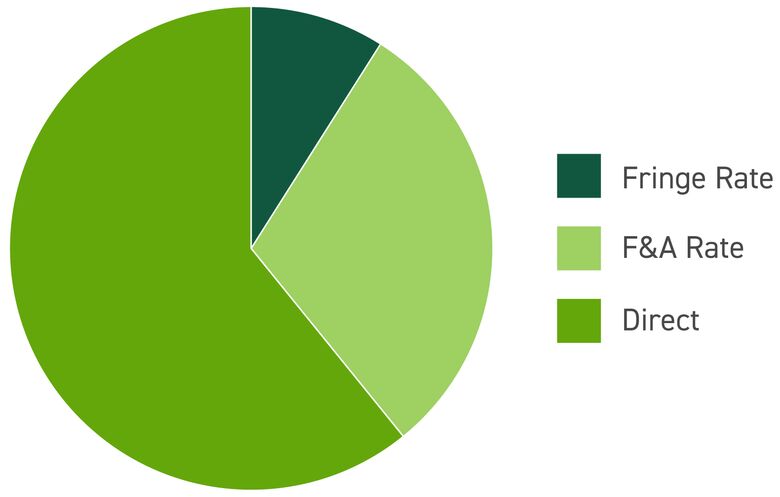

In this next scenario, let’s assume you allocate approximately 50% of your time to the project and the remainder to these indirect activities. Like you, Steve may also contribute time to business development efforts, including proposal writing, presentations, and coordination with potential subcontractors, as well as managing the other employees, accountants and lawyers.

In contrast, technical staff such as Whitney and Dave remain 100% focused on direct project execution (when not on paid time off). These inexpensive people typically work “in” the business.

In this next iteration, the amount of spending hasn’t changed at all; rather, how the two most expensive people are charging their time. The result is a significant increase in the indirect rates: a 25.4% fringe rate and a 58% F&A rate, which is far more realistic.

How People Charge Their Time Drives Your Indirect Cost Rate

What largely drives your indirect rates is how your highly compensated people charge for their time. Most proposal writers massively underestimate how much time everyone in the organization will be non-billable.

Get the Help You Need on Your Next Cost Proposal

Cherry Bekaert’s government contracting advisors are well-versed in indirect rates and help organizations develop accurate, defensible indirect cost rates and prepare competitive SBIR (and all other) cost proposals.

Learn more about our Free SF-424 Cost Proposal Review or connect with our government funding award advisors.

Related Insights