The Financial Accounting Standards Board (FASB) issued two new Accounting Standard Updates (ASUs) in the fourth quarter of 2024. The Government Accounting Standards Board (GASB) issued one new GASB Statement in the fourth quarter of 2024. The latest issue of the Rundown features a summary of the new standards issued. For summaries of standards issued in previous periods, view our previous rundowns here. In addition, we provide a comprehensive listing of all standards newly effective for calendar year-end December 31, 2024, broken down by public business entities, private entities and December 31st year-end governments. Lastly, we list those standards you should consider adopting early.

Fourth Quarter 2024 Newly Issued Standards

Expense Disaggregation Disclosures

This ASU only applies to public entities. Investors have indicated that more granular information about cost of sales, selling, general and administrative expenses (SG&A), and employee compensation would assist them in better understanding an entity’s cost structure and forecasting future cash flows. As a result, the FASB has released this ASU, which essentially requires an entity to disaggregate their income statement into a more granular presentation for footnote purposes.

For interim and annual reporting purposes, a public entity must disclose in tabular format the amounts spent on the below categories that appear within a “relevant expense caption”. A relevant expense caption is simply any expense caption presented on the face of the income statement and within continuing operations that contains one or more of the below expense categories.

- Purchases of inventory

- Employee compensation

- Depreciation

- Intangible asset amortization

- Depreciation, depletion, and amortization related to oil- and gas-producing activities (DD&A)

A relevant expense caption that consists entirely of one of the expense categories listed above is not subject to additional disclosure because the information presented in the income statement satisfies the disclosure requirements in this update. For example, if depreciation is a separate expense caption on the income statement and it consists entirely of just depreciation, then no additional disclosure would be required. However, if the separate expense caption on the income statement consists of both depreciation and intangible asset amortization, then an entity would be required to separately disclose depreciation and intangible asset amortization in tabular format in the footnotes. Similarly, even though an entity might present other expense captions on the face of its income statement, such as interest expense and income tax expense, if those expense captions do not contain any of the expense categories listed above, then those expense captions do not qualify as “relevant expense captions,” and thus the entity is not required to present a disaggregation in tabular format within the footnotes.

In addition, there are various other expense categories already required to be separately disclosed elsewhere in the footnotes (e.g., impairment charges, gain/losses, etc.) that now must be presented in a tabular format along with the above categories. Moreover, to reconcile “relevant expense captions” per the face of the financial statements to the disaggregated expense footnote, the amendment requires a qualitative description for all other amounts contained within a relevant expense caption that is not specifically disclosed.

Lastly, for both interim and annual reporting periods, an entity is required to disclose total selling expenses recognized in continuing operations, and for annual reporting purposes, only an entity shall disclose how it defines the term “selling expenses”.

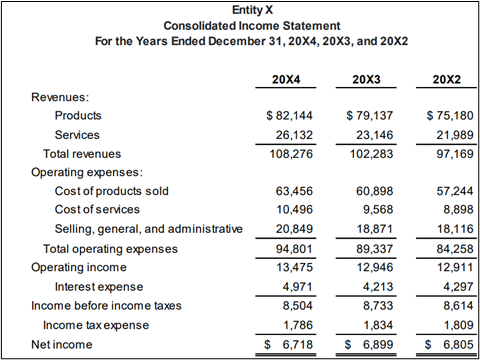

For example, an entity might present the following expense captions in their income statement:

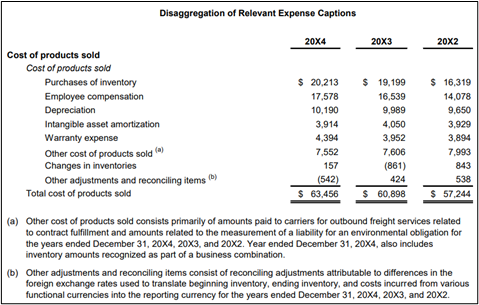

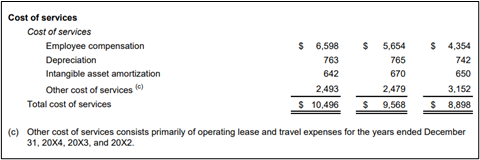

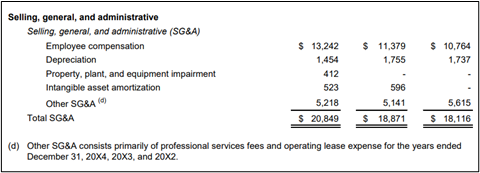

For such an entity, the tabular footnote presentation of disaggregated expenses might look like this:

Effective Date and Transition Requirements:

Public business entities: Annual reporting periods beginning after December 15, 2026, and interim periods beginning after December 15, 2027

All other entities: Not applicable

Early adoption is permitted. The amendments can be applied retrospectively or prospectively.

Induced Conversions of Convertible Debt Instruments

What is an inducement, and why does it matter? In layman’s terms, an inducement is a limited-time offer, usually initiated by the issuer of a financial instrument, to “sweeten” the existing terms and “induce” the holders to convert or exercise. For example, suppose an entity had convertible debt outstanding that, under the original terms, would convert into 100 shares. In that case, the entity might allow holders to convert into 120 shares if they do so within 30 days. It matters because ordinarily, any settlement of debt not pursuant to the original terms would require the entity to determine if the modification should be accounted for pursuant to one of three accounting models: troubled debt restructuring accounting, modification accounting or extinguishment accounting. Moreover, under the extinguishment accounting model, the resulting gain/loss would be computed by taking the difference between the fair value of the cash and/or shares delivered after modification versus the carrying value of the debt. However, if the modification is accounted for as an inducement, then the loss would be computed by taking the difference between the fair value of the cash and/or shares delivered pursuant to the inducement offer versus the cash and/or shares that would’ve been transferred pursuant to the original terms. This latter value is usually much higher than the carrying value, and thus, the loss would be much less.

This amendment clarifies the requirements for determining whether certain settlements of convertible debt instruments should be accounted for as an induced conversion. To qualify for inducement accounting, the offer must meet all of the following criteria:

- Must be available for only a limited period of time

- Provide the holder with more value than they would’ve received pursuant to the original terms

- Be in the same form (e.g., cash, shares, etc.) issuable under the original conversion privileges

This last criterion (i.e. same form) is particularly important. For example, if convertible debt was originally convertible into 100 shares worth $200 ($2/share) and $50 of cash ($250 total value pursuant to original terms), but the settlement offer was for only 200 shares ($400 in value) or only for $400 in cash, then even though the holder would receive more value than the original terms would call for because that value is not in the same form (mix of cash and shares) as the original terms called for, it would not qualify for inducement accounting.

Lastly, the amendment also clarifies two other questions:

- Inducement accounting can apply to convertible debt that is not currently convertible pursuant to the original terms.

- The addition, elimination, or modification of a volume-weighted average price (VWAP) formula does not automatically cause a settlement to be accounted for under the extinguishment model.

Effective Date and Transition Requirements:

All entities: Annual reporting periods beginning after December 15, 2025, and interim periods within that annual period.

Early adoption is permitted if an entity has adopted ASU 2020-06. The amendments can be applied retrospectively or prospectively. Under the prospective transition approach, an entity should apply the amendments to any settlements of convertible debt instruments that occur after the effective date of the guidance. Under the retrospective transition approach, an entity should recast prior periods and recognize a cumulative-effect adjustment to equity as of the later of (1) the beginning of the earliest period presented and (2) the date the entity adopted the amendments in Update 2020-06. In other words, an entity is not permitted to retrospectively apply the amendments in this Update to settlements that occurred before the adoption of ASU 2020-06.

Disclosure of Certain Capital Assets

Statement 104 requires the following types of capital assets to be disclosed separately in the capital asset footnote required by Statement 34:

- Lease assets recognized under Statement 87 Leases

- Intangible right-to-use assets recognized under Statement 94 Public-Private and Public-Public Partnerships and Availability Payment Arrangements

- Subscription assets recognized under Statement No. 96, Subscription-Based Information Technology Arrangements

In addition, intangible assets other than the three types above should be disclosed separately by major class.

Statement 104 also requires additional disclosures for capital assets held for sale. A capital asset is considered held for sale if:

- the government has decided to pursue sale

- it’s probable that the sale will be finalized within one year of the financial statement date

Statement 104 requires disclosure of:

- the ending balance of assets held for sale

- the carrying amount of debt for which the assets held for sale are pledged as collateral

The requirements of GASB 104 are effective for fiscal years beginning after June 15, 2025. Early adoption is encouraged.

List of Newly Effective Standards

Calendar Year-end Public Companies

The following ASUs are effective for public companies for calendar year 2024:

- ASU 2021-01: Reference Rate Reform: Scope

- ASU 2022-06: Reference Rate Reform: Deferral of Sunset Date

- ASU 2020-06*: Debt-Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging-Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity

- ASU 2022-03: Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions

- ASU 2022-04**: Disclosure of Supplier Finance Program Obligations

- ASU 2023-01: Common Control Leasing Arrangements

- ASU 2023-02: Accounting for Investments in Tax Credit Structures Using the Proportional Amortization Method

- ASU 2023-07: Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures

Calendar Year-end Private Companies

The following ASUs are effective for private companies for calendar year 2024:

- ASU 2021-01: Reference Rate Reform: Scope

- ASU 2022-06: Reference Rate Reform: Deferral of Sunset Date

- ASU 2020-06*: Debt-Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging-Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity

- ASU 2021-08: Accounting for Contract Assets and Contract Liabilities from Contracts with Customers

- ASU 2022-01: Fair Value Hedging – Portfolio Layer Method

- ASU 2022-04**: Disclosure of Supplier Finance Program Obligations

- ASU 2023-01: Common Control Leasing Arrangements

Governmental Entities

The following GASB is effective for governmental entities for the calendar year-end December 31, 2024:

Standards Not Yet Effective*, But That You Should Consider Early Adopting, If Applicable

- ASU 2022-03: Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions

- ASU 2023-02: Accounting for Investments in Tax Credit Structures Using the Proportional Amortization Method

- ASU 2023-05: Recognition and Initial Measurement of Joint Ventures

- ASU 2023-08: Accounting for and Disclosure of Crypto Assets

- ASU 2024-01: Compensation—Stock Compensation (Topic 718): Scope Application of Profits Interest and Similar Awards