Key Takeaways

- The NAIC issued final guidance for NAIC REF 2019-21.

- The NAIC definition notes that a bond is a security that creates a creditor relationship with a fixed payment schedule and qualifies as an issuer credit or asset-backed security.

- The PBBP emphasizes economic substance over the legal structure.

- This guidance impacts annual statement schedules and transitionary disclosure for 2025.

The National Association of Insurance Commissioners’ (NAIC) Statutory Accounting Principles Working Group (SAPWG) has finalized the adoption of NAIC REF 2019-21, also known as the Principles-based Bond Project (PBBP), which will significantly impact SSAP No. 26R, Bonds, No. 43R, Asset-Back Securities and No. 21R, Other Admitted Assets, through the adoption and definition of principles-based bonds. The change is effective January 1, 2025, to provide insurance companies sufficient time to implement the guidance and ensure accurate, compliant reporting. The SAPWG issued Issue Paper No. 169 as well as INT 44019 to assist with interpreting and implementing the new bond definition.

The new guidance requires insurers to reassess their bond portfolios and creditor relationships, which will involve changes to reporting structures, risk-based capital ratios and possible reclassification of investments. To ensure compliance for 2025, insurers may need assistance navigating these regulatory changes and maintaining accurate reporting.

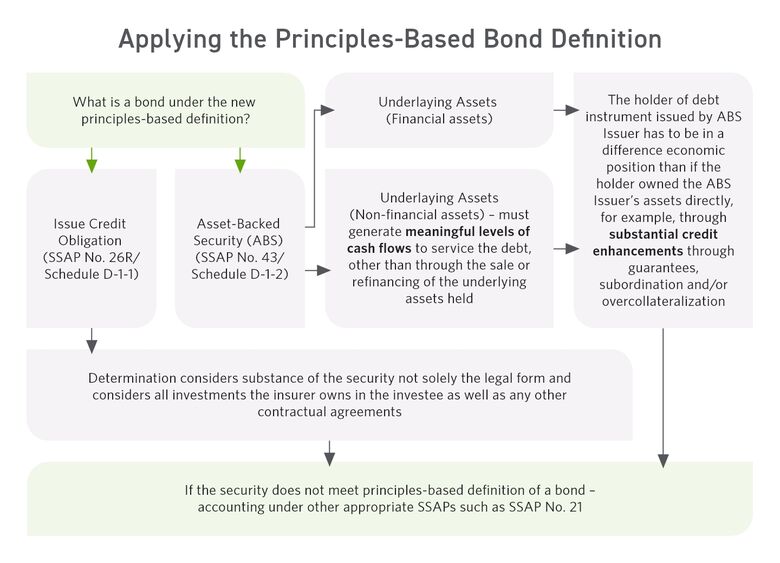

Determining Issuer Credit Obligations vs. Asset-backed Securities: NAIC Principles-based Definition

Under the principles-based bond approach, the revised SSAP No. 26R (5) states:

“A bond shall be defined as any security* representing a creditor relationship, whereby there is a fixed schedule for one or more future payments, and which qualifies as either an issuer credit obligation or an asset-backed security as described in this statement.”

The insurer evaluating a creditor relationship should primarily consider the security's substance, rather than the legal form of the financial instrument. Additionally, all other investments the insurer owns in the investee, as well as any other contractual arrangements, should be included within the consideration and analysis over the existing relationship. A creditor relationship exists when a security has predetermined principal and fixed or variable interest payments that do not vary based on the performance of underlying collateral or non-debt variables. Furthermore, securities that represent an ownership interest or that possess equity-like characteristics are not, in substance, bonds.

Consider this example, presented during NAIC implementation discussions, which involved a security collateralized by both mortgage‑backed securities and artwork. Under the principles‑based bond definition, the analysis focuses on whether the structure represents a creditor relationship supported by meaningful, recurring cash flows and whether repayment is primarily tied to an operating entity or underlying collateral. In this case, even if part of the collateral consists of cash‑flowing financial assets, the inclusion of artwork — which does not independently generate meaningful cash flows — prevents the security from meeting the criteria for either an issuer credit obligation or an asset‑backed security. As a result, the instrument does not qualify as a bond under the revised guidance and would default to reporting on Schedule BA. This example highlights how certain mixed or unconventional collateral structures that may have qualified for bond treatment under prior SSAP 43 guidance will no longer meet the principles‑based definition.

Defining Issuer Credit Obligations

Under the principles-based bond approach, the revised SSAP No. 26R (7) also details:

“An issuer credit obligation is a bond, for which the general creditworthiness of an operating entity or entities through direct or indirect recourse, is the primary** source of repayment.”

Examples of issuer credit obligations include, but are not limited to:

- U.S. Treasury securities, including U.S. Treasury Inflated-protected Securities (TIPS)

- U.S. government agency securities

- Municipal securities

- Corporate bonds issued by operating entities and issued by holding companies that own operating entities, including zero-coupon bonds

- Project finance bonds issued by operating entities

- Bonds issued by real estate investment trusts (REITs)

- Bonds issued by business development corporations

- Convertible bonds issued by operating entities, including mandatory convertible bonds as defined in the revised SSAP No. 26R paragraph 20.b.

Clarifying Asset-backed Securities

The revised SSAP No. 43R, Asset-Backed Securities, defines:

“An asset-backed security is a bond issued by an entity (an ABS Issuer) created for the primary purpose of raising debt capital backed by financial assets or cash generating non-financial assets owned by the ABS Issuer, for which the primary source of repayment is derived from the cash flows associated with the underlying defined collateral rather than the cash flows of an operating entity***. In most instances, the ABS Issuer is not expected to continue functioning beyond the final maturity of the debt initially raised by the ABS Issuer.”

For a bond to be considered an asset-backed security (ABS), the assets owned by the ABS Issuer are either financial assets or cash-generating non-financial assets. Cash-generating, non-financial assets are assets expected to generate a meaningful level of cash flow toward repayment of the bond, and must also have a meaningful level of cash flow to service the debt, other than through the sale or refinancing of the underlying assets held by the ABS Issuer.

As a practical expedient, a reporting entity may consider an asset for which less than 50% of the original principal relies on sale or refinancing to meet the meaningful criteria. In applying this practical expedient, only contractual cash flows of the non-financial assets may be considered.

Examples of asset-backed securities include, but are not limited to:

- Residential Mortgage-backed Securities (RMBSs)

- Commercial Mortgage-backed Securities (CMBSs)

- Collateral Loan Obligations (CLOs)

- Other Asset-backed Security Financial Instruments

- Auto Loan-backed Securities

- Credit Card-backed Securities

- Lease-backed Securities

- Student Loan-backed Securities

- Equipment Lease-backed Securities

Understanding the Impact of NAIC Bond Project Guidance on Your Insurance Company

Based on the guidance released thus far, these initial changes will mainly impact annual statement schedules, coupled with a transitionary disclosure required only to file for the first quarter of 2025. As your insurance company undergoes its reporting procedures, pay close attention to the following updates:

- Schedule D will be divided into two parts:

- Schedule D Part 1, Section 1: Long-term Bonds — Issuer Credit Obligations Owned

- Schedule D Part 1, Section 2: Asset-backed Securities Owned

The reporting categories of each part of Schedule D have been updated to conform with changes made by the Blanks Working Group (BWG).

- Schedule BA explains that included securities will need to be re-evaluated based on the principles-based definition as noted within the revised SSAP No. 26R.

- Risk-based capital (RBC) ratios may be impacted based on the potential shift of reporting between Schedule D and Schedule BA.

Reporting Impacts

This guidance indicates that any assets previously listed under Schedule D must be reclassified to appropriate schedules, like Schedule BA. Generally, during this transition from Schedule D to Schedule BA, they should be recorded at their amortized cost. Any assets reported at fair value under Schedule D as of December 31, 2024, must reverse any unrealized adjustments on January 1, 2025, and be removed from Schedule D. It is important to understand that dropping an asset from Schedule D will not result in any recognized gain or loss.

Upon transitioning an asset to Schedule BA, it should be reported at an amortized cost and then valued correctly for Schedule BA, though this may lead to unrealized losses. However, the asset’s new, book-adjusted carrying value should never exceed its amortized cost due to unrealized gains. Transitioning and recognizing an asset to Schedule BA ensures appropriate and accurately updated financial records from period to period.

Making Adoption Considerations

Effective January 1, 2025, insurers should evaluate their Schedule D assets and adjust their assessments to ensure appropriate reporting for 2025 quarterly and annual statements. Insurers should account for data requirements needed to evaluate their Schedule D securities, the time required to accurately assess their classification under the bond standard, as well as their holdings’ natures and complexities. For securities not meeting the new bond-based definition, prepare a supporting schedule for reclassification to Schedule BA. With the new guidance, insurers identifying classification changes should also consider RBC impacts and their future investment strategy to proactively avoid or alleviate potential issues.

The NAIC has also published various materials pertaining to these principles-based bond updates, such as this Q&A document and Statutory Issue Paper No. 169, to help make industry leaders aware of these changes. Stay connected with your advisor as the NAIC releases additional guidance within the 2025 disclosure checklists or otherwise.

Let Us Guide You Forward

Cherry Bekaert’s Insurance team has a wide range of resources and industry professionals to assist you when evaluating your bond portfolios to identify which securities are issuer credit obligations or asset-backed securities and determine if the financial instrument no longer qualifies as a bond and would instead be reported within Schedule BA.

Additionally, we can work with management teams to evaluate their internal control environment and whether the insurer has properly categorized investments held on the quarterly and annual statements to meet regulatory requirements.

The guidance is effective January 1, 2025, and reporting will be required in the first quarterly statement of 2025. Contact a Cherry Bekaert advisor today to help your insurance company prepare for this regulatory shift and assist with accurate reporting.

Notes:*This statement adopts the GAAP definition of a security as it is used in FASB Accounting Standards Codification Topics 320 and 860. Evaluation of an investment under this definition should consider the substance of the instrument rather than solely its legal form.**“Primary” refers to the first in order of repayment source, not to a majority of the sources of repayment.***Dedicated cash flows from an operating entity can form the underlying defined collateral in an asset-backed security. This dynamic, perhaps noted in a whole-business securitization, still reflects an asset-backed security and is not an issuer credit obligation.

Related Insights