The Forces Reshaping the U.S. Banking Industry

The U.S. banking industry is undergoing one of its most consequential structural transformations in decades, due to a combination of macroeconomic pressures, technological disruption, regulatory recalibration, and evolving consumer expectations that are reshaping the competitive landscape.

Several powerful structural forces will define the industry’s trajectory through 2030:

- Accelerating bank mergers and acquisitions (M&A)

- Continued macroeconomic volatility

- Evolving regulatory and tax policy frameworks

- Rapid adoption of artificial intelligence (AI)

- Expanding competition from neobanks and fintech

- Emergence of open banking and financial data portability

- Large-scale technology modernization initiatives

- Growth of embedded finance ecosystems

- Escalating threats from cybercrime and financial fraud

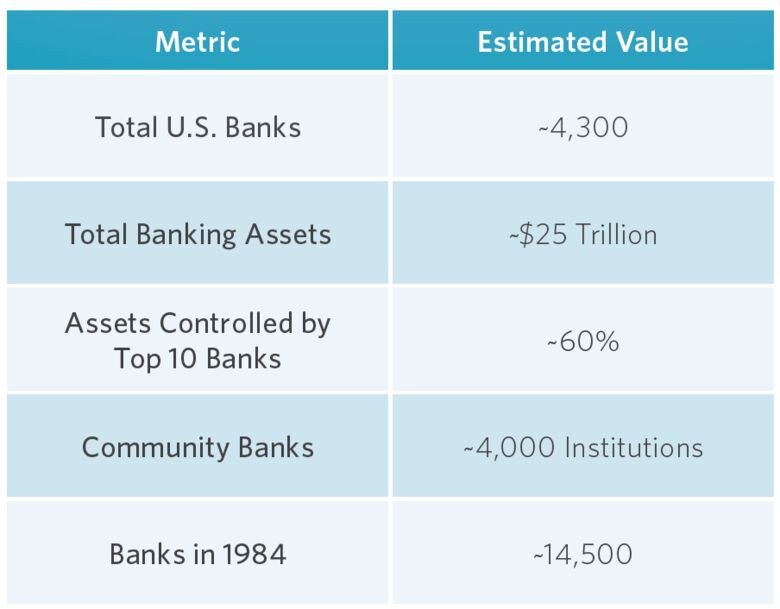

Despite the size and global influence of the U.S. banking system, the industry remains fragmented. Approximately 4,300 banks operate nationwide, although the largest institutions control a disproportionate, and still growing, share of total assets. This fragmentation, combined with escalating technology investment requirements, is accelerating consolidation and strategic partnerships.

At the same time, banks face unprecedented competition from fintech platforms and digital-native financial institutions. These competitors are redefining the customer experience through mobile-first interfaces, embedded financial services and data-driven personalization. Technological disruption is another defining challenge for institutions. AI is rapidly expanding across banking functions — from fraud detection and credit underwriting to compliance monitoring and customer service.

Smaller community and regional banks face an even more complex strategic landscape, shaped by consolidation forces, economic uncertainty and evolving policy dynamics. M&A is increasingly viewed both as a growth opportunity and a survival strategy, as rising technology costs, regulatory complexity and intense competition make scale more critical. Industry observers note that banks under roughly $1 billion in assets face growing pressure either to specialize or consider consolidation as maintaining independence becomes more difficult.

Banks that successfully integrate technological innovation, operational efficiency and strong risk management will be best positioned to thrive in the evolving financial landscape.

“As financial institutions of all sizes navigate consolidation forces, technological evolutions,

rising consumer demands, mounting regulatory pressures, and pivotal succession planning tactics, only those brave enough to embrace innovating in stride with these pressures will thrive.”

Industry Structure and Market Concentration: Bigger, Fewer, Stronger?

The U.S. banking industry is one of the largest and most complex financial systems in the world, with total assets exceeding $25 trillion as of 2025. It includes thousands of institutions ranging from small community banks to globally systemic financial institutions. Despite this large number of participants, the industry’s structure is highly uneven, combining a long “tail” of small institutions with a small group of dominant players at the top.

U.S. Banking Industry Structure

A defining feature of the modern U.S. banking sector is its high and increasing market concentration. The largest institutions control a disproportionate share of assets: the 10 biggest banks alone account for roughly 60% of total industry assets, while just 1% of banks hold nearly 70% of all assets.

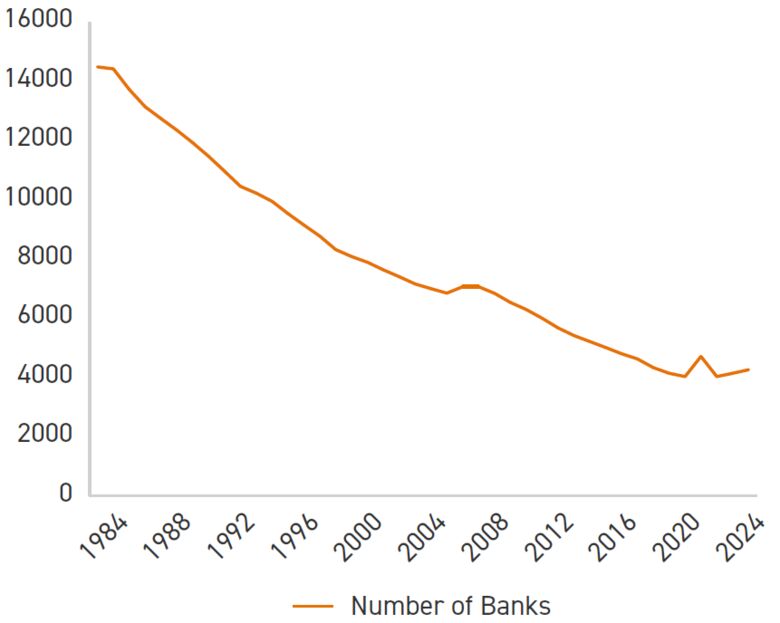

This trend reflects decades of consolidation driven by deregulation, economies of scale, technological investment and merger activity. This concentration has accelerated since the 1980s, when there were over 14,000 banks, compared to fewer than 5,000 today.

At the same time, the industry remains highly fragmented beneath the top tier. Community banks — representing roughly 90–96% of all institutions — play a critical role in local economies, particularly in small business, agricultural and rural lending. However, their share of total assets has steadily declined to a relatively small portion of the system, highlighting the growing divide between large, diversified financial institutions and smaller, relationship-driven banks with the impacts of that divide felt most heavily in smaller and/or rural communities across the country.

Overall, the U.S. banking industry’s evolving structure reflects a dual dynamic: increasing consolidation and scale at the top, alongside persistent fragmentation at the community level. This bifurcated model continues to shape competition, regulation, and risk in the financial system, with large banks benefiting from scale and diversification, while smaller banks remain essential to localized lending and economic development.

The Great Consolidation: M&A Reshapes U.S. Bank Landscape

Consolidation has become one of the most defining trends in the banking industry, which is in the middle of a historic consolidation wave — one that is redrawing the competitive map, squeezing smaller institutions and accelerating the rise of a new class of financial giants.

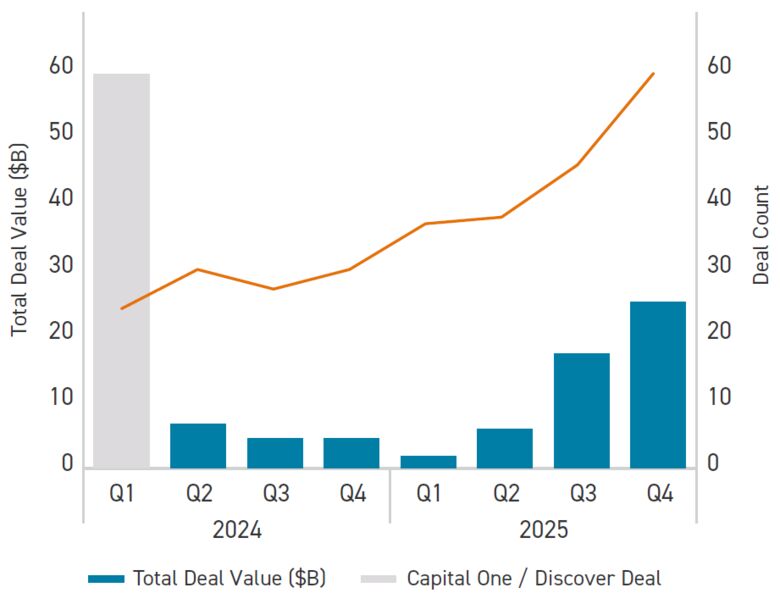

After several false starts, 2025 delivered a clear rebound in U.S. bank M&A, with deal volume and values up sharply from recent years. Announced deals exceeded 2024 totals, and aggregate transaction value moved decisively higher, with activity spanning traditional community and regional bank mergers as well as targeted acquisitions of niche platforms.

The momentum shows no signs of slowing, with 180+ deals announced in 2025 and monthly tally reaching $21.4 billion in October — the highest single month since early 2019 — bank M&A entered 2026 with a rare alignment of favorable market conditions and a more permissive regulatory environment.

U.S. Bank Consolidation: FDIC-insured Commercial Banks (1984-2025)

While there are several converging forces fueling this consolidation surge, perhaps the most powerful driver is the widening technology gap between large and small institutions. Over the past 15 years, banks have increased their technology spending by about 65% and are expected to grow these budgets by roughly 10% yearly over the next five years. As of 2023, the largest banks’ technology budgets are more than 10 times those of regional banks, a differential that continues to widen. The rise of AI has made this gap even more acute. In 2026, the cost of maintaining a competitive AI-driven banking platform has become a “table stakes” expense that community and mid-sized banks can no longer afford on their own.

A friendlier regulatory climate has also contributed to the consolidation trend. The prior administration took a restrictive approach to bank mergers, but that has changed dramatically. The current regulatory regime has adopted a softer, more deregulatory stance, with key actions, including:

- Easing capital requirements

- Rolling back select consumer-protection rules

- Proposing to raise the threshold for the strictest supervisory standards from $50 billion to $700 billion in assets

- Most recently in December 2025, increasing FDICIA regulatory thresholds to match inflation and reduce compliance costs for smaller banks that previously crossed these thresholds solely due to inflation

In addition, with interest rates stabilizing and loan growth slowing, many mid-sized banks see M&A as a route to bolster profitability through cost cuts and efficiency. Merging allows branch overlaps to be eliminated and backoffice operations to be consolidated, yielding significant expense savings.

But a growing share of U.S. bank M&A is being driven less by traditional scale economics and more by a quieter, structural issue: succession planning. Thousands of community and regional banks remain closely held, often with aging leadership teams and concentrated ownership among founders or long-tenured executives. As these leaders approach retirement, many institutions face a limited internal bench capable, or willing, to take over. Recruiting external leadership is costly, uncertain and increasingly difficult given regulatory complexity and margin pressure. In that context, a sale becomes a practical exit strategy rather than a purely strategic expansion decision.

This dynamic is especially pronounced among smaller banks, where the CEO may also be a major shareholder and central to client relationships, credit culture and local market knowledge. Without a clear successor, boards are forced to weigh the risks of leadership gaps against the certainty of a sale to a larger, better-resourced institution. M&A offers liquidity for shareholders, continuity for customers and a transition path for employees, while avoiding the disruption that can come with an unproven leadership change.

As a result, succession-driven M&A is becoming a key, if understated, catalyst of consolidation. It tends to produce a steady pipeline of smaller, often off-market deals rather than headline-grabbing mergers, but its cumulative effect is significant: a gradual reduction in the number of independently operated banks and a continued shift toward larger, more diversified institutions.

“As consolidation in the banking industry accelerates and national institutions gain scale, smaller regional banks must adapt to keep pace. They will need to innovate to stay competitive and M&A is increasingly becoming an existential requirement.”

Landmark Deals Reshaping the Landscape

The scale of recent transactions underscores just how transformative this wave has been. Capital One’s $35.3 billion acquisition of Discover Financial sent a clear signal that regulators are growing more open to megadeals. At the regional level, the $10.9 billion merger of Fifth Third Bancorp and Comerica, along with the $7.4 billion purchase of Cadence Bank by Huntington Bancshares, signal an aggressive shift toward a “mega-regional” model designed to rival the scale of the nation’s largest money-center institutions.

For regional and community banks, the picture is more complicated. Mid-sized banks are often unable to afford the tech investments required to compete, creating a widening gulf in service offerings, innovation and customer retention. Many now face a stark choice: find a merger partner, acquire smaller institutions themselves or risk being left behind. Banks with strategic gaps are scouting targets, while underperforming banks are increasingly open to selling. Regional and community banks in particular may find themselves the target of unsolicited inbound offers.

That said, it isn’t all bad news for smaller players. Regional and community banks, which generate the bulk of their earnings from spread-based income, are poised to benefit the most from easing capital requirements. If favorable rates and supportive credit conditions continue, smaller banks should be well positioned to rebound from multiyear valuation lows.

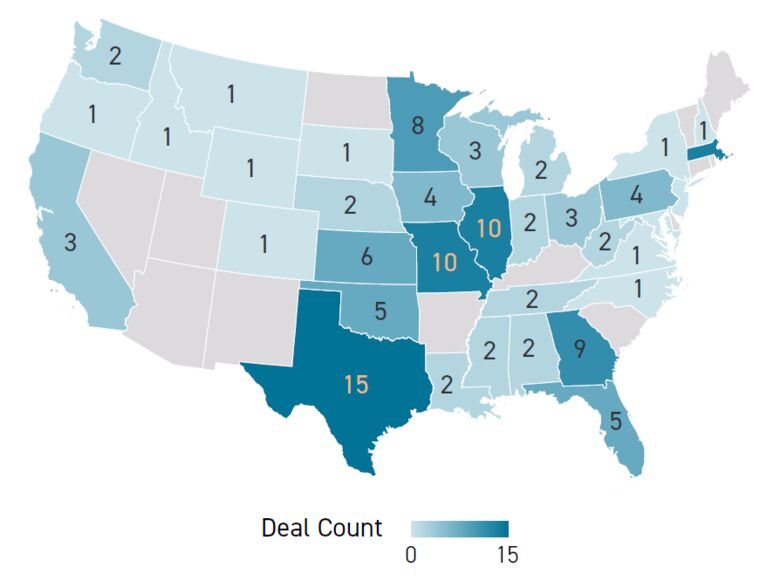

This year will be pivotal for U.S. bank mergers, with positive momentum carrying into 2026 after a sustained flow of banking deals in 2025 signaled a healthy appetite for consolidation. Bank M&A announcements in 2025 reached their highest level since 2021, with 181 deals according to S&P Global Market Intelligence, and the second half of the year saw a surge of 106 announcements compared to 57 in the latter half of 2024. For smaller regional and community banks, the message is clear: scale up, specialize or risk finding yourself at the negotiating table on someone else’s terms.

2025 U.S. Bank M&A Deal Count by Target State

As of: 10/2025

Announced U.S. Bank M&A Deal Count and Combined Value

Macroeconomic Realities Facing Banks

The U.S. banking industry in 2026 is operating from a position of relative strength, but against a backdrop of meaningful macroeconomic uncertainty and structural change. Key macroeconomic pressures include:

- Deposit competition: Depositors increasingly seek higher-yield alternatives, including money market funds and digital savings platforms.

- Loan demand moderation: High borrowing costs have dampened demand in several lending segments, particularly commercial and industrial. Commercial real estate lending has picked up in anticipation of lower rates.

- Balance sheet volatility: Rising rates created unrealized losses on fixed-income securities held by many banks.

- Commercial real estate risk: Office market valuations remain under pressure due to persistent remote-work trends.

Profitability remains solid — industry return on equity is expected to hover around 11 – 12% — supported by stillhealthy credit conditions and prior expansion in net interest margins. Simultaneously, the operating environment has become more complex, shaped by elevated but shifting interest rates, persistent inflationary pressures and uneven economic growth. These dynamics are forcing banks of all sizes to reassess balance sheet strategy, funding models and long-term positioning.

One of the most significant challenges is the interest rate environment and its impact on funding and profitability. A relatively flat or inverted yield curve — where short-term funding costs approach or exceed long-term lending yields — has compressed margins and complicated asset-liability management. Deposit competition has also intensified, with customers seeking higher yields and alternative vehicles, including money market funds and emerging digital assets. This pressure is particularly acute for small and regional banks, which rely more heavily on deposit funding and lack the diversified revenue streams of larger institutions. In addition, asset quality risks are beginning to rise modestly, with some regional banks facing weaker credit performance in certain loan portfolios.

Regulation and policy are also in flux, adding both opportunity and uncertainty. Recent proposals to ease capital requirements could lower funding constraints and free up capital for lending, dividends and strategic investment across banks of all sizes. However, these changes remain controversial, with critics warning they could increase systemic risk over time. For regional banks, the regulatory outlook is mixed: while some relief is expected, new rules may require greater recognition of unrealized losses and more rigorous risk management following the failures seen in 2023.

The near-term outlook for the banking industry is best described as cautiously constructive. Following the aggressive interest-rate tightening cycle implemented by the Federal Reserve (Fed) between 2022 and 2024, the industry is adapting to a sustained higher-rate environment. However, expectations of potential rate cuts could ease funding pressures and stabilize margins, while overall economic conditions remain resilient but uncertain. Larger banks are likely to continue benefiting from scale, diversification, and regulatory flexibility, while smaller and regional institutions face a more challenging path: balancing margin pressure, competition for deposits and ongoing structural change. Ultimately, the industry’s trajectory will depend on the interplay between macroeconomic conditions, regulatory direction and how effectively banks execute on transformation initiatives already underway.

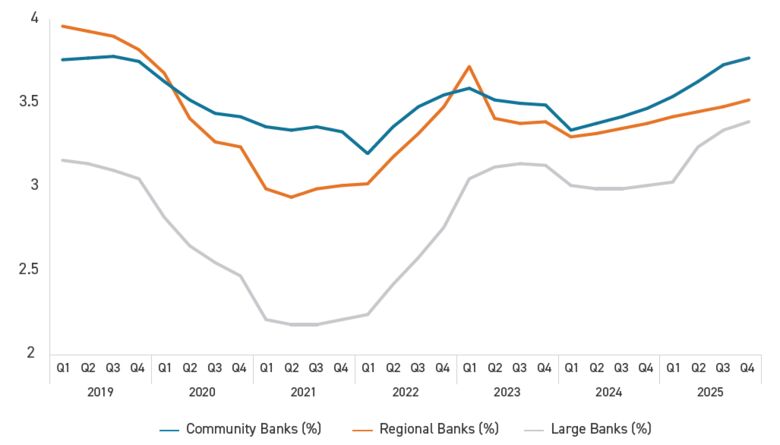

Banking Net Interest Margins

Key U.S. Tax Policy Developments Shaping the Industry

U.S. tax policy developments continue to shape the operating environment for the banking industry, with several reforms reinforcing a broadly pro-growth and business-friendly fiscal framework.

A central development is the extension and modification of provisions originally enacted under the 2017 tax overhaul signed by President Donald Trump. Many of these policies were extended and/or expanded through the 2025 reconciliation legislation known as the “One Big Beautiful Bill Act,” (OBBBA) which preserved lower corporate and individual tax rates and extended several investment incentives.

The continuation of the 21% corporate tax rate, along with the permanent extension of key business deductions, supports bank profitability and capital formation by maintaining favorable after-tax returns on investment and lending activity. The introduction of Section 139L creates a favorable dynamic for agricultural lending, particularly within rural markets, but the benefit must be evaluated in the context of interest expense limitation calculations, which will partially offset the intended tax advantage reinforcing the need for careful modeling to determine the true after-tax benefit.

Other tax policy developments affecting banks involve changes to pass-through taxation and incentives that directly influence the structure and capital planning of financial institutions. The reconciliation legislation permanently extended the Section 199A qualified business income deduction, allowing eligible pass-through entities — including many community and regional banks organized as S-corporations (roughly 30% of all U.S. commercial banks) — to deduct up to 20% of qualified income. Without this extension, the effective tax rate on pass-through income could have risen significantly, potentially encouraging restructuring toward C-corporation status. The preservation of this deduction helps maintain competitive tax parity between organizational structures and supports capital retention among smaller banks, which rely heavily on internal capital generation to fund lending growth.

Additional tax policy developments affecting the banking sector include new excise taxes and modifications to international tax rules that may indirectly shape financial flows and bank services. The reconciliation legislation introduced a 1% excise tax on certain cross-border remittances beginning in 2026, which may alter the economics of international payment services offered by banks and fintech firms.

Collectively, these evolving tax policies illustrate how fiscal policy is increasingly intertwined with financial sector strategy, influencing bank organizational structures, capital allocation decisions, cross-border activity, and the competitive dynamics between traditional banks and emerging financial technology providers.

“The future of tax policy remains uncertain, as partisan provisions are vulnerable to changes in congressional and executive control and the United States faces mounting fiscal pressure and upcoming tax cliffs. For banks, that means planning can’t rely on permanence – institutions that plan dynamically, rather than reactively, are better positioned to navigate both opportunity and risk.”

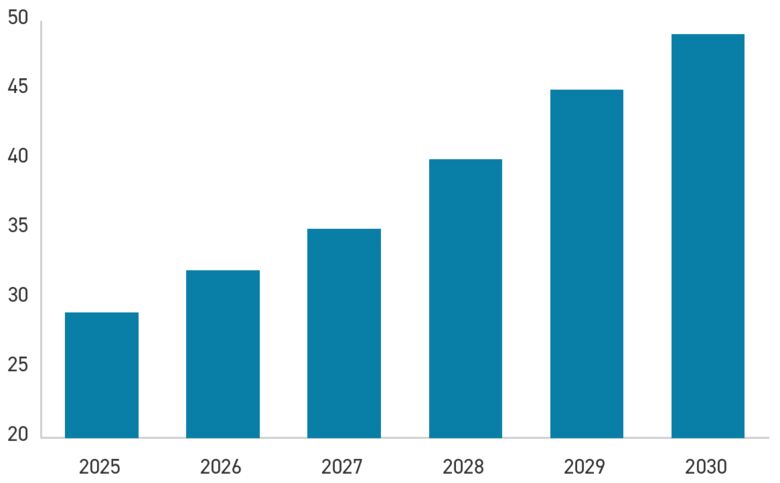

Artificial Intelligence and the Future of Banking

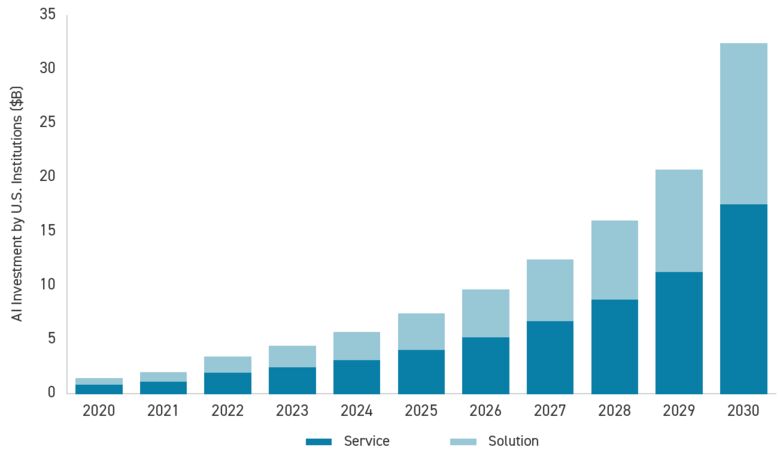

Artificial intelligence is rapidly transforming financial services. According to a report published by Grand View Research, a market research and consulting company, global spending on artificial intelligence solutions within the banking sector was estimated at $19.87 billion in 2023 and is projected to reach over $143 billion by 2030, growing at a CAGR of 31.8% from 2024 to 2030. AI integration in banking has transformed the sector, strengthening a more customercentric approach and enhancing technological relevance.

The Twin Pillars of AI Risk: Why Data Governance and Third-party Management Can’t Wait

As artificial intelligence becomes embedded across enterprise platforms, two risk areas are emerging as critical blind spots for the industry: data governance and third-party (vendor) risk management. Far from being isolated compliance concerns, these issues are now deeply intertwined with how organizations adopt and oversee AI and the stakes are rising fast.

Today, virtually every technology vendor is releasing its own version of AI, embedding it directly into the platforms organizations already rely on. The problem is that not all of these implementations come with adequate guardrails. Businesses may find themselves using AI-powered features without fully understanding how their data is being processed, retained or exposed. This makes vendor management no longer just a procurement or IT concern, but a frontline risk management issue.

Organizations need to scrutinize AI capabilities in every vendor contract with the same rigor applied to data security and privacy provisions. Institutions must move beyond simply evaluating vendors for compliance to assess how they are using institutional data with AI and what safeguards are in place.

Compounding the vendor challenge is a structural shift in how data is stored. The era of centralized, in-house data management is largely over. Today, data is distributed across multiple cloud platforms, third-party services, and softwareas-a-service (SaaS) applications — a reality that significantly amplifies cyber and financial crime risk. Each node in that ecosystem represents a potential point of exposure, and the attack surface grows with every new integration.

This distributed environment makes data governance not just a regulatory checkbox but an operational necessity. Without clear policies governing where data lives, who can access it, and how AI systems interact with it, organizations are navigating blind.

Given these converging threats, third-party risk management and data governance deserve prominent placement in any organization’s strategic risk framework. They should be treated not as back-office functions but as enterprise-level priorities with executive visibility and dedicated resources.

The organizations that move proactively — building robust vendor oversight programs and enforcing strong data governance policies before incidents occur — will be far better positioned as AI adoption accelerates. Those that wait may find themselves managing crises instead of opportunities.

“In a digitally driven banking world where data flows freely across clouds and vendors, vigilant data governance and third-party risk management are cornerstones to solidify and maintain stakeholder trust, profitable growth and scalable for integration and innovation.”

Key AI Banking Trends and Insights

Market Overview

- Credit underwriting North America dominated AI in banking with a share of 37.8% in 2025.

- Compliance monitoring Based on AI segmentation, the solution segment (i.e., AI models that aim to solve specific business problems) dominated the market with a revenue share of 59.6% in 2025.

- Based on application, risk management (i.e., AI models that solve risk or vulnerability) accounted for the largest market revenue share in 2025.

- Based on technology, natural language processing (NLP) accounted for the largest market revenue share in 2025.

Market Size and Forecast

- The 2025 market size totaled $23.77 billion

- The projected market size for 2030 is $143.56 billion

- The compound annual growth rate (CAGR) from 2024 – 2030 is projected to be 31.8%

- North America remains the largest market in 2025

U.S. Artificial Intelligence in the Banking Market

As of: 11/20/2025

Competition From Fintech and Neobanks

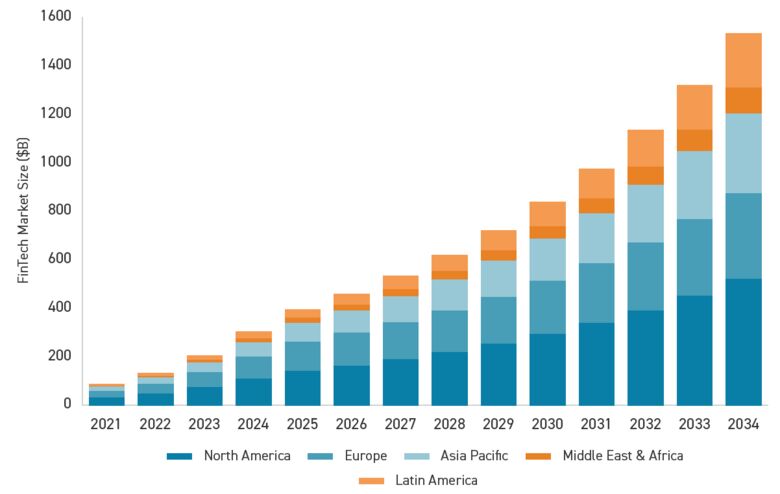

Fintech companies have significantly expanded their presence in financial services according to recent industry projections from multiple research firms, including Polaris Market Research. The global fintech market is estimated to become a $1.5 trillion industry by 2034 in terms of revenue generation, and financial institutions are leading the way with digital innovations.

Digital banks offer:

- Fee-free accounts

- Intuitive mobile experiences

- Instant payments

- Integrated financial tools

Global Fintech Revenue Forecast

As of: 3/2026

“Customer loyalty is no longer solely tied to institutions through familial and interpersonal relationships but instead, increasingly values seamless, personalized user experiences. Successful institutions must adapt alongside these shifts to ensure they remain trusted partners to a younger generation.”

Open Banking and Data Ownership

Open banking is reshaping financial services by enabling consumers to share financial data with thirdparty applications, such as financial management platforms, digital lending, automated savings tools and integrated payments.

Open banking will likely evolve into open finance, expanding data sharing to insurance, investments and pensions. With widespread sharing becoming more commonplace, the control of financial data may become one of the most important competitive advantages in banking.

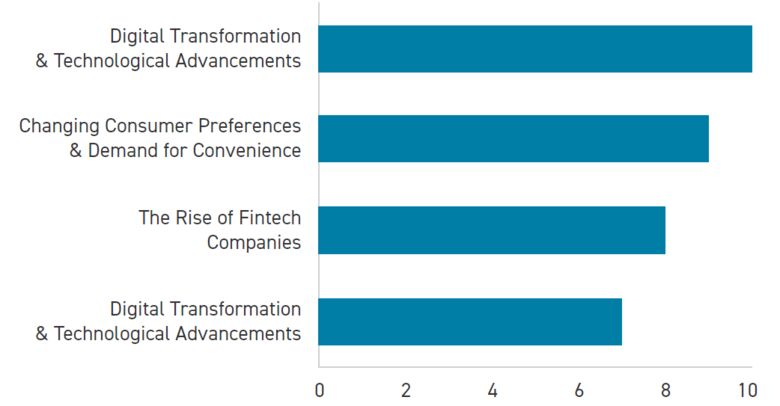

U.S. Retail Banking Market Drivers

As of 12/2025

Operational Modernization

Modernizing operations is at the forefront of digital disruptions, as legacy technology systems remain one of the greatest challenges facing traditional banks. With outdated software and systems, banks may face siloed data, slow manual processes and inhibited decision-making, leading to lost growth opportunities. Key modernization initiatives include:

- Cloud migration

- API-driven infrastructure

- Modular core banking systems

- Advanced data analytics platforms

Banks are expected to spend over $1 trillion annually on digital transformation initiatives by the late 2020s, highlighting the importance of these initiatives. Particularly with the rising use of automation, modern technology platforms are essential to remain competitive and support tools like AI applications, real-time payments, and open banking ecosystems.

Embedded Finance and Banking-as-a-Service

Embedded finance is one of the fastest-growing areas in financial services with middle-market community banks at the forefront, thanks in large part to the Durbin Amendment advantage, which caps interchange fees on debit transactions for banks with $10B+ in assets at roughly 21 – 24 cents per transaction, while banks below that threshold remain exempt and can charge the full market rate, typically 44 – 55 cents per transaction. This has created a structural economic advantage that has made community banks indispensable partners in the embedded finance and BaaS ecosystem.

When a fintech — say, a neobank, buy now, pay later (BNPL) provider, or payroll platform — wants to issue debit cards, they need a chartered bank sponsor. If that sponsor is a large institution, every swipe generates capped interchange revenue. But partnering with a community bank under $10B means the fintech (and its bank partner) can share in full, uncapped interchange economics, which is often the primary revenue engine for card-based fintech products.

This is precisely why banks like Bancorp Bank, Sutton Bank, Pathward (MetaBank), and Cross River Bank became foundational infrastructure providers: they monetize the regulatory exemption at scale by sponsoring hundreds of fintech programs.

Beyond interchange, community banks bring the actual regulatory charter, the most valuable and difficult-toreplicate asset in financial services. They handle Bank Secrecy Act and Anti-money Laundering (BSA/AML) compliance obligations, FDIC insurance pass-through, and state licensing coverage, allowing fintechs to operate without obtaining their own charter (an expensive, years-long process).

This results in a symbiotic relationship where fintechs provide distribution and technology while community banks provide regulatory infrastructure and economics. A small bank in Kentucky or Pennsylvania can effectively power millions of consumer accounts nationally without opening a single branch, which fundamentally redefines what “community banking” means in the modern era.

Financial products are increasingly integrated into non-financial platforms such as:

- E-commerce marketplaces

- Ride-sharing apps

- Enterprise software platforms

- Digital marketplaces

Through banking-as-a-service, banks provide regulated infrastructure while technology companies manage customer relationships. This model allows financial services to appear everywhere consumers interact digitally.

“As banking-as-a-service models scale, banks are being asked to innovate while maintaining regulatory discipline. The winners will be institutions that can support fintech growth without losing control over risk, compliance, and governance.”

Cybersecurity and Financial Crime

Cybersecurity threats continue to escalate, and financial institutions have increasingly become major targets. Banks face ever-increasing digital risks including ransomware, phishing attacks, identity fraud and AI-generated scams.

The financial services cybersecurity systems and services market is expected to see rapid growth in the next few years, expanding to an anticipated $49.06 billion in 2030 at a CAGR of 10.9%.

The growth in the forecast period can be attributed to increasing investments in AI-powered cybersecurity tools, as threats become more sophisticated and banks move to enhance security measures to mitigate the risks. Rising demand for secure digital payment ecosystems and the expansion of open banking platforms will also drive market expansion, since the nature of these systems creates increased risk of data breaches and application programming interface (API) vulnerabilities, among other risks. Overall, the industry is experiencing a growing focus on proactive threat intelligence, causing an increase in cybersecurity spending by financial institutions.

Financial Services Cybersecurity Systems Market ($B)

U.S. Bank Industry Outlook

The American banking industry is navigating one of its most consequential periods in decades. Consolidation, deregulation, digital disruption and macroeconomic uncertainty are converging simultaneously to reshape strategy, competition and survival across institutions of every size.

The long-anticipated merger wave has finally arrived in force. The banking sphere saw a surge in consolidation in 2025, with some analysts predicting 2026 could see double that amount, given pent-up pressure and a much quicker regulatory evaluation period. Landmark deals have signaled regulators’ growing openness to megadeals.

The logic is simple: scale has become a survival mechanism. The largest banks’ technology budgets are more than 10 times those of regional banks, and this differential continues to widen. Merging allows institutions to spread those costs, eliminate branch overlaps and build the capital buffers needed to compete. Smaller banks may find their “buyer universe” shrinking as the midsize lenders they once counted on as potential acquirers become acquisition targets themselves.

2030 Banking Outlook

Several structural changes are likely to define the next phase of the U.S. banking industry.

With federal regulatory agency leaders reshaping their approach to supervision, and the industry preparing for, potentially, the most significant changes to the capital framework in more than a decade, 2026 is poised to be a watershed year for banking regulation. Key among the changes is a proposal to raise the threshold for the strictest supervisory standards from $50 billion to $700 billion in assets, dramatically lightening the compliance load for hundreds of regional institutions.

Tax policy adds another tailwind. Tax reform has the potential to return meaningful cash to the system — some provisions may increase cash in the hands of consumers and businesses, influencing loan demand, while others may encourage capital investment and related financing activity. For banks seeking loan growth, a tax-driven lift in business and consumer spending could provide incremental support to top-line performance. However, the ultimate impact will be shaped by broader economic uncertainty and the pace at which borrowers translate tax savings into activity.

Technology is moving from experiment to infrastructure in 2026. Artificial intelligence is the most transformative force in the industry, with more than 70% of banking firms using agentic AI to some degree. The upside is vast — some analysts estimate generative AI could add $200 billion to $340 billion annually to global banking, primarily through efficiency gains — but execution remains the challenge. Banks whose data infrastructure is fragmented or legacybound may struggle to scale AI meaningfully, ceding ground to more digitally mature competitors.

The economic backdrop appears to be one of tempered optimism. The baseline scenario according to S&P Global projects GDP growth at roughly 2.2% in 2026, marking a stabilization or slight up-tick compared to the 2.1% growth observed in 2025. In a downside scenario, tariff impacts and other geopolitical instability could stall GDP or push it briefly negative.

Lower rates are expected to squeeze net interest margins, especially for banks reliant on deposit funding and floating-rate lending. But higher fees, commissions and deposit repricing may serve as offsets, keeping profitability broadly stable.

Credit quality remains manageable, though tighter consumer lending standards and modest unemployment risks bear watching.

The institutions best positioned for 2026 are those moving decisively on M&A, AI infrastructure, digital assets and fee diversification. Banks that build strong fee-based businesses in wealth management, capital markets, embedded finance, and digital payments will be better insulated against interest rate cycles.

The choices made this year will not just determine who wins this cycle; they will define the competitive order of U.S. banking for the decade ahead.