A compliant job cost report is one of the most important tools a government contractor can have. Using a sample NIH SBIR Phase I award, this article breaks down how a job cost report works, what it tracks, and why it matters for your bottom line and your next funding opportunity.

What Is a Job Cost Report and Why Does It Matter?

A job cost report is a financial document that gives you a clear, complete picture of your project expenditures to show how award monies were spent. In government contracting, job cost reports are a critical management and compliance tool because they provide visibility into how labor, materials and other costs are charged to each contract, enabling accurate billing, regulatory compliance and informed decision-making.

In summary, job cost reports:

- Calculate revenue earned each month.

- Track actual spending versus budgeted amounts in your award.

- Monitor the amount earned as compared to the amount drawn.

- Serve as a management tool for you and the awarding agency.

As a government contractor, you must maintain your accounting system in accordance with Federal Acquisition Regulation (FAR) Part 31, and the job cost report is reliable proof that your system meets that standard — helping you control risk, protect margins and demonstrate accountability to government customers.

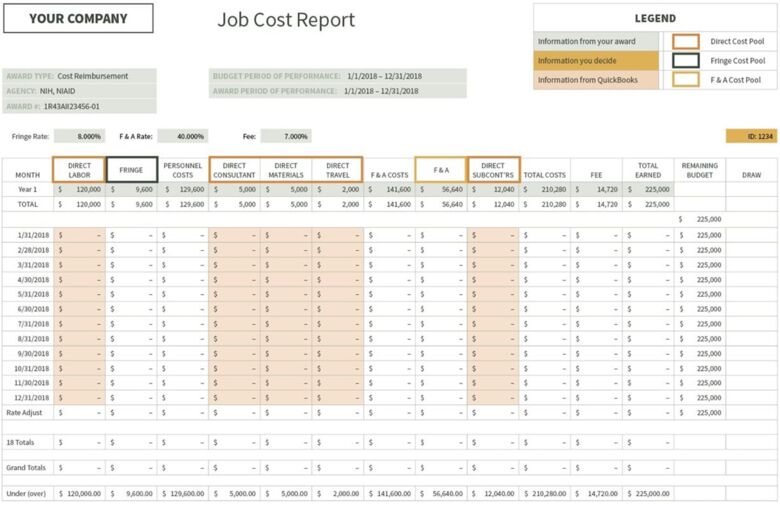

We’ve created a sample QuickBooks report to show you how a job cost report looks and works, and how it satisfies federal government requirements. In this example, we are using a National Institutes of Health (NIH) Small Business Innovation Research (SBIR) Phase 1 award of $225,000, with a fringe benefit rate of 8%, facilities and administrative (F&A) rate of 40% and a fee of 7%.

Tracking Spending by Cost Category

To be compliant with the FAR and avoid potential issues at audit, you must segregate your expenditures into three different cost pools:

- Direct costs

- Indirect costs (in this example, fringe and F&A costs)

- Unallowable costs

It is critical that you keep your books in such a way that these cost pools are easily identified. These cost pools should also be maintained on a monthly basis.

Fig. 2 (below) is a close-up of the columns in the job cost report shown in Fig. 1, which demonstrates this.

Direct Costs

You are required to accumulate your direct costs — specific costs that you’ve identified as solely benefiting this one particular project only. These costs are pulled directly from your accounting system and are indicated by the blue-shaded sections.

Indirect Costs

Next comes your indirect costs (fringe and F&A). These numbers are based on the indirect cost rates, which may need to be approved by the Division of Financial Advisory Services (DFAS) and can be found in your award. Fringe and F&A are defined as follows:

- Fringe is the cost of having employees — payroll taxes, vacation, holiday and sick time, medical benefits, and so on.

- F&A is facilities and administration — the costs required to run your business, such as rent, telephone, utilities, accounting, HR and legal services.

Unallowable Costs

Unallowable costs do not appear on the job cost report. They are costs that the government will not reimburse you for and are tracked separately in the general ledger.

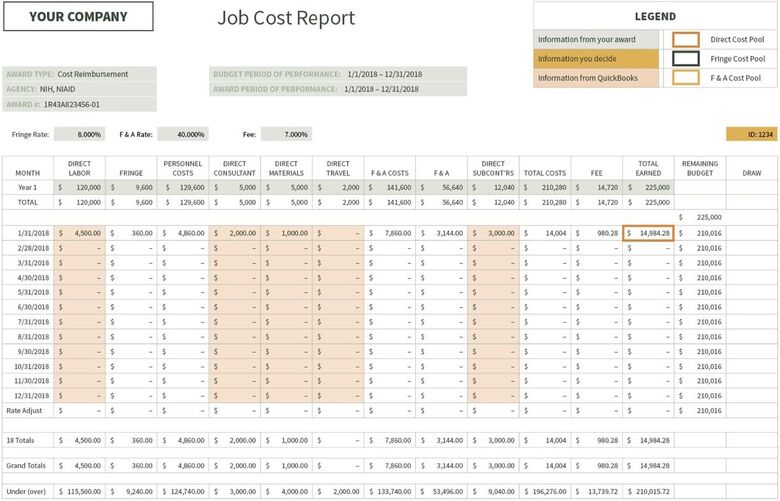

The job cost report calculates the revenue earned each month.

Once you’ve entered your direct costs, your fringe, F&A and fee will calculate based on your award provisional rate. These numbers will be allocated to each job proportionate to their direct costs.

In the job cost report above, you’ll see the following: direct labor $4,500 + your 8% fringe rate = $4,860. This is your total direct personnel costs.

Next:

- Add the other direct costs, which make up your F&A costs base (consultants, materials, travel) of $3,000 to get your F&A costs base of $7,860.

- Add your 40% F&A rate of $3,144 and your direct subcontractor costs of $3,000 to get your total costs of $14,004.

- Add your 7% fee of $980.28 and your total expenditure to get how much of your $225,000 award money you’ve earned: $14,984.28

The job cost report tracks actual spending versus budgeted amounts in your award.

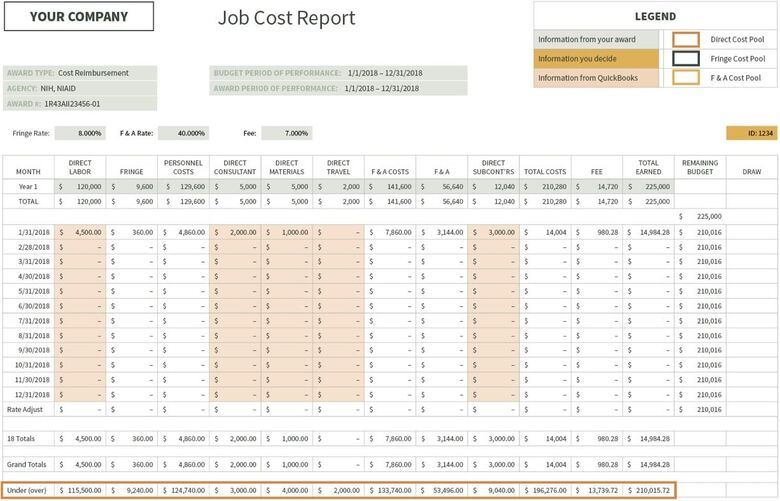

When you submit your SBIR Phase I proposal, you give the NIH important budgetary projections, such as how much you would spend on direct labor, materials, consultants, subcontractors and travel. You also allocate a fair and reasonable fringe benefit rate, F&A rate and fee. These projections are indicated in the Year 1 line.

Scroll down to the bottom of the following job cost report, to the very last line, “Under/Over.” This clearly shows whether you are under or over your budgeted amount, and by how much. It also gives you a great way to track your spending and make critical adjustments as you progress through your Phase I award. Know that most government funding awards allow you to re-budget between direct cost-categories with limitations. You need to be familiar with this option.

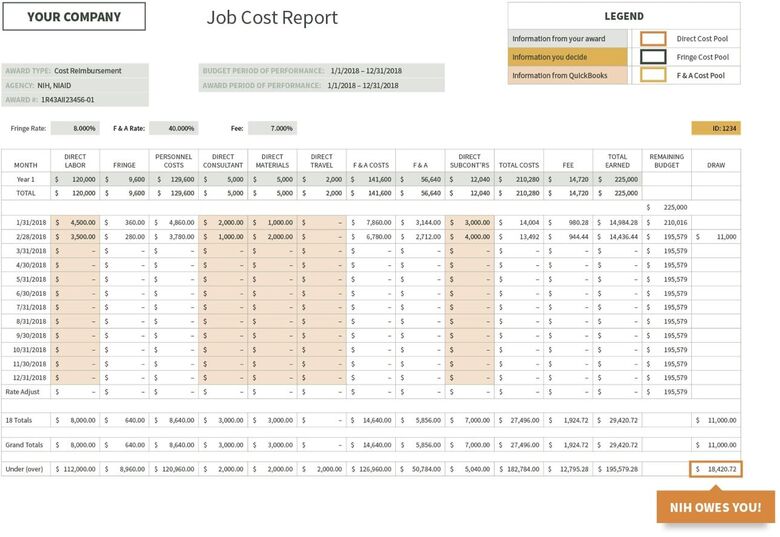

Use the job cost report to monitor the amount earned as compared to the amount drawn.

In this example, you’ve earned $29,420.72 of your award monies, but you’ve only drawn $11,000. Therefore, at this stage in your NIH funding, you have underdrawn $18,420.72.

Issues With Overdrawing and Underdrawing

Assuming you always draw for direct expenses, if your job cost report shows that you are over or underdrawing, it’s most likely caused by a difference in your provisional fringe and/or F&A rate versus your actual fringe and/or F&A costs.

In the example above, our NIH grantee has underdrawn on grant funds by $18,420.72. There may be several good reasons for this, including:

- They prepaid for items and need to be reimbursed.

- They haven’t had the indirect expenses to draw down for yet, but they will.

- They are drawing for actual indirect expenses but have miscalculated their F&A rate, and it’s running much lower than 40%.

We advise clients to just keep an eye on it. If you see a pattern, such as your rate is chronically high or low, then you need to take the following actions:

- If you are chronically underdrawn, then you need to re-budget from your F&A budget to your direct budget. There are constraints, so make sure you consult with a government contracting advisor. At the end of the day, you want to spend all of your grant funds. Don’t leave money on the table.

- If you are chronically overdrawn and you do not have outside funding, then you have to get your expenditures under control. Otherwise, you will owe money to your funding agency for all overdrawn indirect expenses. The federal government expects to be repaid for an overdraw of indirect expenses. Without an indirect rate agreement that says otherwise, you are not allowed to re-budget from a direct cost category to an indirect cost category.

Your job cost report is a management tool for you and the awarding agency.

For you to move on and receive Phase II funding in this example, you must demonstrate to the awarding agency that you maintain a FAR Part 31 compliant accounting system. The job cost report is primary proof that you are ready for more fiscal responsibility.

If you can’t demonstrate a compliant job cost report, you’re telling them the exact opposite.

Your Guide Forward

A FAR-compliant job cost report is a foundational tool for effective oversight and long-term success in government contracting. Clear visibility into costs, budget performance, and award drawdowns helps you manage risk, support compliance, and demonstrate financial discipline to awarding agencies. To strengthen your reporting approach and position your organization for future funding, connect with Cherry Bekaert’s government contracting advisors.

Related Insights